.png)

.webp)

.webp)

.webp)

For a $500M company, every five days of excess DSO locks up roughly $6.8 million in working capital. That is not a process bottleneck. That is infrastructure, product development, and talent acquisition that never happens because capital is trapped inside your receivables.

The pressure is compounding. CFOs are being asked to deliver cash predictability, scale operations without adding headcount while managing risk in real time.

Credit and accounts receivable sit at the center of every one of those demands.

Growfin partnered with the Credit Research Foundation (CRF) for a live session on how AI agents are transforming the credit-to-cash lifecycle. Timothy Ray, VP of Global Sales at Growfin, walked through the forces driving this shift, the structural problem that traditional finance models cannot solve, and the practical use cases where agentic AI is already delivering measurable results for finance teams.

Here are the key takeaways.

1. Why Credit and AR Are Under More Pressure Than Ever

Credit and accounts receivable have become the front line of enterprise cash flow performance. Finance leadership is being pushed to deliver more with less margin for error, and the pressure is coming from every direction simultaneously.

According to Deloitte, 84% of CFOs expect rising cost pressures over the next year, with cost control and cash management ranking as their top priorities. Working capital efficiency is no longer a finance operations concern. It is a board-level priority.

That pressure is not abstract. It translates into specific, compounding demands on every finance team responsible for credit decisions and cash collection.

Four forces are converging on finance teams at once:

- Mandate to scale without increasing headcount,

- Non-negotiable expectations around cash predictability and accuracy

- Need for real-time risk management with proactive decisioning

- Organizational push to adopt AI as a growth enabler

According to Gartner research referenced during the session, demand for AI in credit and AR has grown 3x since 2023, driven by increasing pressure on finance leaders to improve cash flow, risk visibility, and operational efficiency.

Yet according to a Kyndryl study, 71% of finance leaders either acknowledge AI's value but are not ready to trust it fully, or actively oppose it.

That gap between pressure and readiness is where the opportunity sits.

2. The Real Problem Is Structural, Not Operational

Credit and AR hold some of the most valuable risk and cash data in the enterprise, yet in most organizations, those signals never connect. That disconnect is the root cause of AR and credit underperformance, not the speed at which teams work.

Five Symptoms of a Legacy AR + Credit Model

- Functional silos where teams work independently with limited shared visibility

- Critical data is spread across fragmented systems

- Decisions rely on periodic, retrospective reporting cycles

- Workflows depend heavily on manual execution

- Policies follow static rules that cannot adapt to changing customer behavior

The problem deepens when you look at how modern monetization has evolved. Companies now manage diverse billing structures (subscription, usage-based, milestone, hybrid invoicing), customer-specific payment terms shaped by contracts and negotiated agreements, multiple payment channels spanning ACH, wire, check, cards, portals, and lockbox, and fragmented systems of record across CRM, ERP, billing platforms, and banking portals.

The Hidden Cost: Credit and AR Data That Never Talks

Modern finance demands the exact opposite: speed, predictability, scale, and real-time visibility across the entire credit-to-cash lifecycle.

But the most costly structural problem is subtler: credit and AR hold valuable data, yet rarely share a unified view.

- Credit teams track credit scores, approved limits, liquidity analysis, customer financial profiles, and industry segment risk.

- AR teams track payment timing, short pays, delinquency trends, dispute volume, and promise-to-pay commitments.

- Cash application teams see partial payments, deductions, and remittance patterns.

- Cash forecasting teams watch portfolio aging trends, DSO, and collection efficiency.

Each of these functions generates risk signals. In most organizations, those signals never connect. A customer whose payment behavior is deteriorating in collections may still be operating on a credit limit that was set during a quarterly review six months ago. A pattern of increasing disputes visible to the cash application team may never reach the credit analyst who could adjust terms proactively.

3. The Paradigm Shift: From Systems of Record to Systems of Action

The central argument of the session was that finance technology must evolve from systems of record to systems of action. Recording transactions and storing data is necessary but insufficient. The next generation of finance platforms needs to act on intelligence, not just display it.

How AI redefines the future of Credit and AR

Generative AI provides the knowledge layer. It is trained on global financial literature, regulatory frameworks, and industry data. Think of it as the equivalent of a highly knowledgeable new hire who understands the domain broadly but has never seen your specific business.

Machine learning adds the context layer. It trains specifically on your industry's dynamics, your customer base, and your payers' behavioral patterns. This is the equivalent of that new hire spending months learning how your customers actually pay, which accounts are seasonal, and which dispute types recur.

Agentic actions complete the execution layer. This is automation that acts on the intelligence from generative AI and ML the way a trained, experienced collector acts independently: making judgment calls about which accounts to prioritize, adjusting dunning strategies based on customer response patterns, and escalating only when a situation genuinely requires human decision-making.

Human judgment and oversight remain essential for exceptions. The system does not replace finance professionals. It removes the repetitive manual burden so they can focus on the decisions that require experience, relationship context, and nuance.

The shift is not "automation versus humans." It is a three-layer architecture: generative AI for knowledge, machine learning for context, and agentic execution for action, with human oversight governing exceptions. The result is a system of collaboration, not replacement.

Five trends already reshaping credit-to-cash lifecycle

Autonomous credit scoring replaces periodic, spreadsheet-based credit reviews with AI-driven, real-time credit decisions that include confidence scoring.

Conversational AR enables finance professionals to ask natural-language questions and receive instant, data-backed answers across their entire receivables portfolio, no report building required.

Dispute root-cause engines auto-classify disputes by root cause and recommend resolutions, replacing manual investigation cycles.

Predictive collections segments and prioritizes accounts for follow-up based on live behavioral signals, not static aging buckets.

Touchless cash application automates payment matching with minimal manual effort, handling high-confidence matches autonomously and routing only true exceptions to human reviewers.

4. What Unified, Agentic Credit-to-Cash Looks Like in Practice

When AI is applied across the full credit-to-cash lifecycle instead of to isolated point solutions, four capabilities emerge that are impossible to achieve with disconnected tools.

Real-time customer risk context. Credit bureau data, financial signals, and behavioral indicators feed into continuous credit risk monitoring, enabling dynamic policy optimization and proactive limit and term adjustments. Instead of quarterly portfolio reviews, risk is monitored from day one.

Actionable payment signals. Payment behavior, dispute patterns, and follow-up responsiveness become live inputs to collections strategy, not lagging indicators reviewed after the fact.

Continuous cash flow visibility. Cash forecasting operates on a feedback loop with live receivables data, achieving forward-looking accuracy rather than backward-looking reporting.

Closed-loop decisioning. Insights from credit risk flow into collections prioritization, which flows into cash application intelligence, which feeds back into credit policy, creating a self-improving cycle.

How Growfin Brings Unified Credit-to-Cash Intelligence to Life

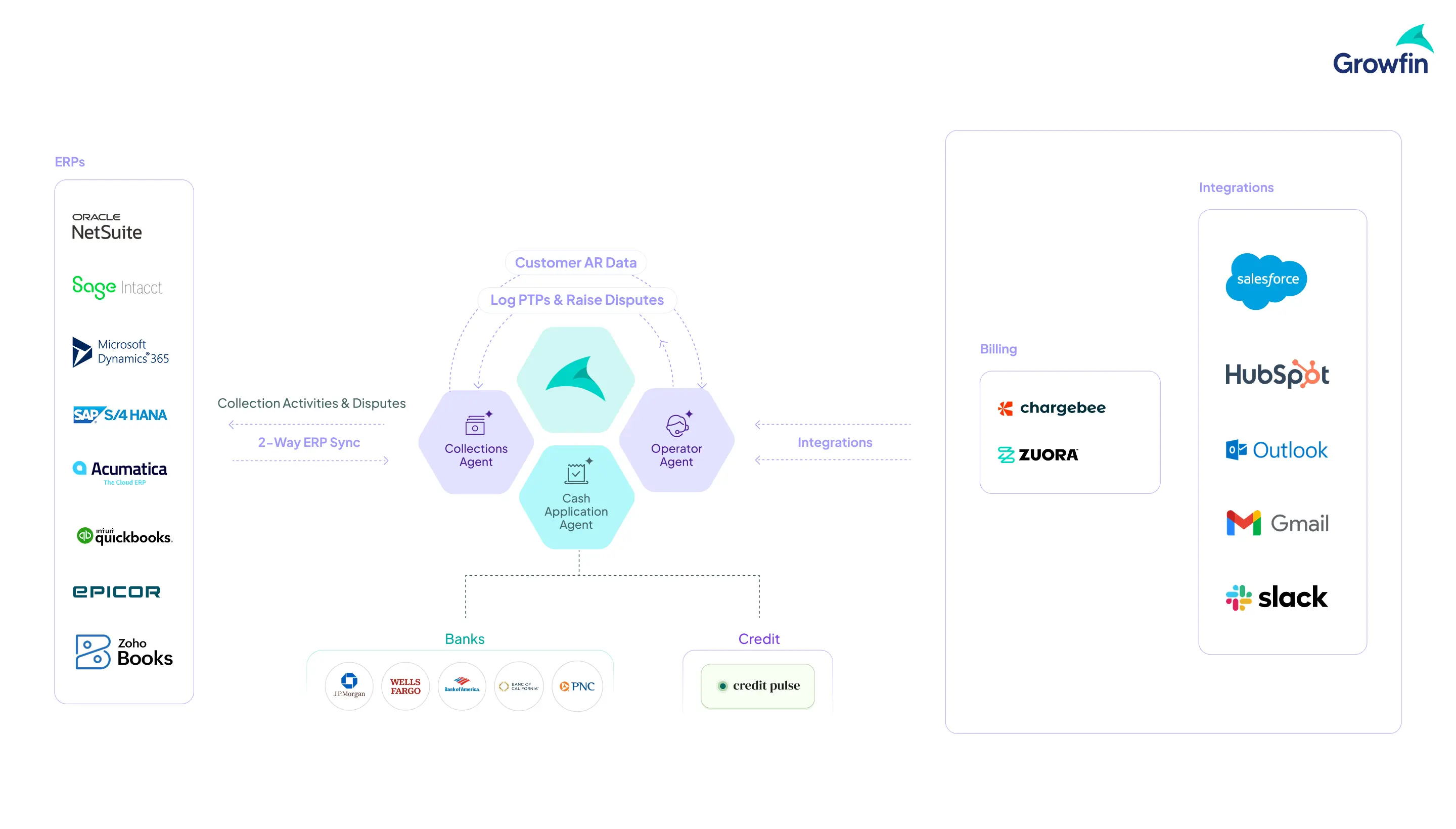

These four capabilities describe what becomes possible when credit and AR operate as a single intelligent system. Growfin's agentic architecture is purpose-built to deliver exactly this: AI agents that operate across the credit-to-cash lifecycle while connecting natively to the systems finance teams already use.

That includes ERPs (NetSuite, Sage Intacct, Microsoft Dynamics 365, SAP S/4HANA, and others), CRMs (Salesforce, HubSpot), billing platforms (Chargebee, Zuora), banking systems, and communication tools (Outlook, Gmail, Slack).

Growfin's agentic architecture brings this to life through purpose-built AI agents that operate across the credit-to-cash lifecycle while connecting natively to the systems finance teams already use: ERPs (NetSuite, Sage Intacct, Microsoft Dynamics 365, and others), CRMs (Salesforce, HubSpot), billing platforms (Chargebee, Zuora), banking systems, and communication tools (Outlook, Gmail, Slack).

Three agents work together within this architecture:

The Collections Agent executes personalized dunning strategies autonomously. It analyzes each customer's payment behavior, suppresses reminders that historical data shows are ineffective for that account, and adapts strategy in real time. If a customer typically pays 4-6 days after the invoice due date and rarely responds to automated pre-due reminders, the agent recognizes this pattern and shifts to a personalized follow-up timed for maximum impact.

The Cash Application Agent handles complex, real-world payment scenarios: partial payments, combined invoices, payments from entities operating under different names, and unstructured remittance data. It automates high-confidence matches, escalates genuine exceptions to human reviewers, and learns continuously from every correction.

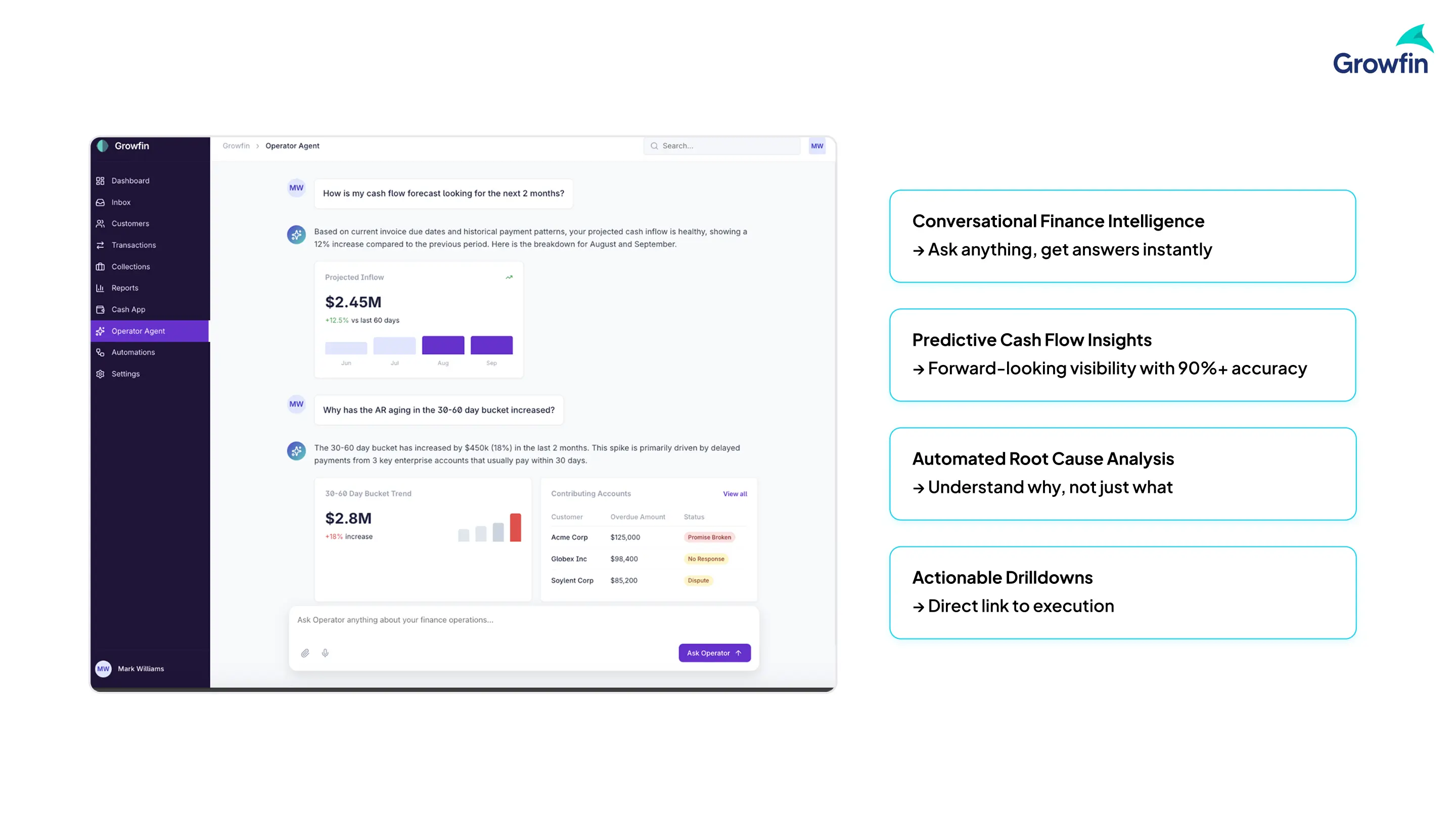

The Operator Agent provides conversational finance intelligence. Finance leaders can ask natural-language questions ("How is my cash flow forecast looking for the next 2 months?" or "Why has the AR aging in the 30-60 day bucket increased?") and receive instant, data-backed answers with drilldowns to contributing accounts and root causes.

The architecture above shows what is possible. The question most finance leaders ask next is practical: how do we actually get there? The adoption path matters as much as the technology itself, because AI in credit and AR is a progression, not a switch.

5. How to Start: The Adoption Path That Works

AI adoption in credit and AR is a progression, not a switch. Organizations that try to jump straight to full autonomy without building the foundational layers will struggle with data quality, team trust, and change management. The session outlined a five-phase path that maps to how successful finance teams are actually making this transition.

Phase 1: Identify high-impact outcomes. Start with the use cases that have the clearest, most measurable ROI. For most organizations, that means cash application (highest AI maturity, fastest time to value) or collections prioritization (direct DSO impact).

Phase 2: Unify data across the credit-to-cash lifecycle. Break the silos between credit, collections, cash application, and billing systems. No AI model can make intelligent decisions on fragmented, inconsistent data.

Phase 3: Layer AI into credit decisions, collections prioritization, and cash forecasting. Apply intelligence to the decision points where human analysts currently spend the most time on repetitive analysis.

Phase 4: Embed AI into core workflows. Move from AI-as-insights to AI-as-execution across credit operations, collector workflows, and exception handling. This is where agentic actions begin.

Phase 5: Deploy AI agents that act on insights, orchestrate workflows, and learn continuously. Full agentic execution with human oversight for exceptions. The system improves with every transaction, every correction, and every resolution.

The progression follows a clear logic: Insight, then Decision, then Execution, then Autonomy.

The Credit-to-Cash Moment

Credit and AR have operated as separate functions for decades. Separate teams, separate systems, separate review cycles. That model worked when billing was simple, payment channels were few, and quarterly reviews were fast enough.

None of those conditions hold anymore. The volume, velocity, and complexity of modern receivables demand a unified, intelligent system that connects credit risk to collections execution to cash application to forecasting, in real time, with minimal manual intervention.

That is the system Growfin built. Purpose-built AI agents that unify the credit-to-cash lifecycle, connect natively to the systems finance teams already use, and improve with every transaction.

Book a demo to see our AI agents in action.

TL;DR

- Credit and AR are now the central pressure point for enterprise cash flow, risk management, and liquidity. 84% of CFOs expect rising cost pressures, and demand for AI in credit and AR has tripled since 2023.

- The root problem is structural: credit and AR hold valuable risk signals, but they almost never share a unified view, leading to reactive decisions, missed signals, and millions in trapped working capital.

- Finance technology is shifting from systems of record to systems of action: a three-layer architecture combining generative AI (knowledge), machine learning (context), and agentic execution (action), with human oversight for exceptions.

- Unified credit-to-cash intelligence connects credit risk monitoring, collections execution, cash application, and cash forecasting into a closed-loop system where each function strengthens the others.

- Adoption follows a clear progression: Insight, then Decision, then Execution, then Autonomy. Start with high-impact use cases, unify your data, and build organizational trust before scaling to full agentic execution.

.webp)

.webp)

.webp)

.webp)