.png)

.webp)

.webp)

.webp)

ERP has always been the gravitational center of finance by design. You spent years consolidating entities, rationalizing charts of accounts, and standardizing processes so that one system could serve as the ledger of record. From a governance standpoint, that decision was correct. It reduced reconciliation risk, shortened close, and gave you a single history of what happened.

In Accounts Receivable, it also created a powerful illusion. Once invoices, payments, and adjustments flowed through ERP, it was tempting to assume that AR itself was now “under control.” If AR lived in the same system that satisfied auditors and regulators, surely it could also serve as your real-time view of cash and customer behavior.

That assumption has been largely inaccurate.

Not because your past ERP investments were wrong, but because AR’s job is structurally different from what ERP was built to do. ERP is engineered to finalize history. AR is paid to anticipate future cash and shape risk before it hits the P&L.

The tension shows up in the questions only you see at your level:

- Why do forecast meetings still lean on spreadsheets; and why are they still inaccurate?

- Why does Treasury need AR deadlines before making liquidity decisions?

- Why do AR teams still have multiple systems open while trying to collect cash?

Those are not symptoms of weak discipline or resistant teams. They are symptoms of asking ERP to be something it was never hired to be: an AR system of intelligence.

What ERPs were hired to do, and why AR needs a different brain

ERP’s mandate can be summarized in three questions:

- Did this transaction occur?

- Was it recorded correctly according to policy?

- Can we reconstruct it and defend it?

Everything about ERP’s architecture: strict schemas, batch processing, period locking, audit trails; is tuned for that mandate. It is a system of record for financial history.

Accounts Receivable’s mandate is different. AR must answer more volatile questions:

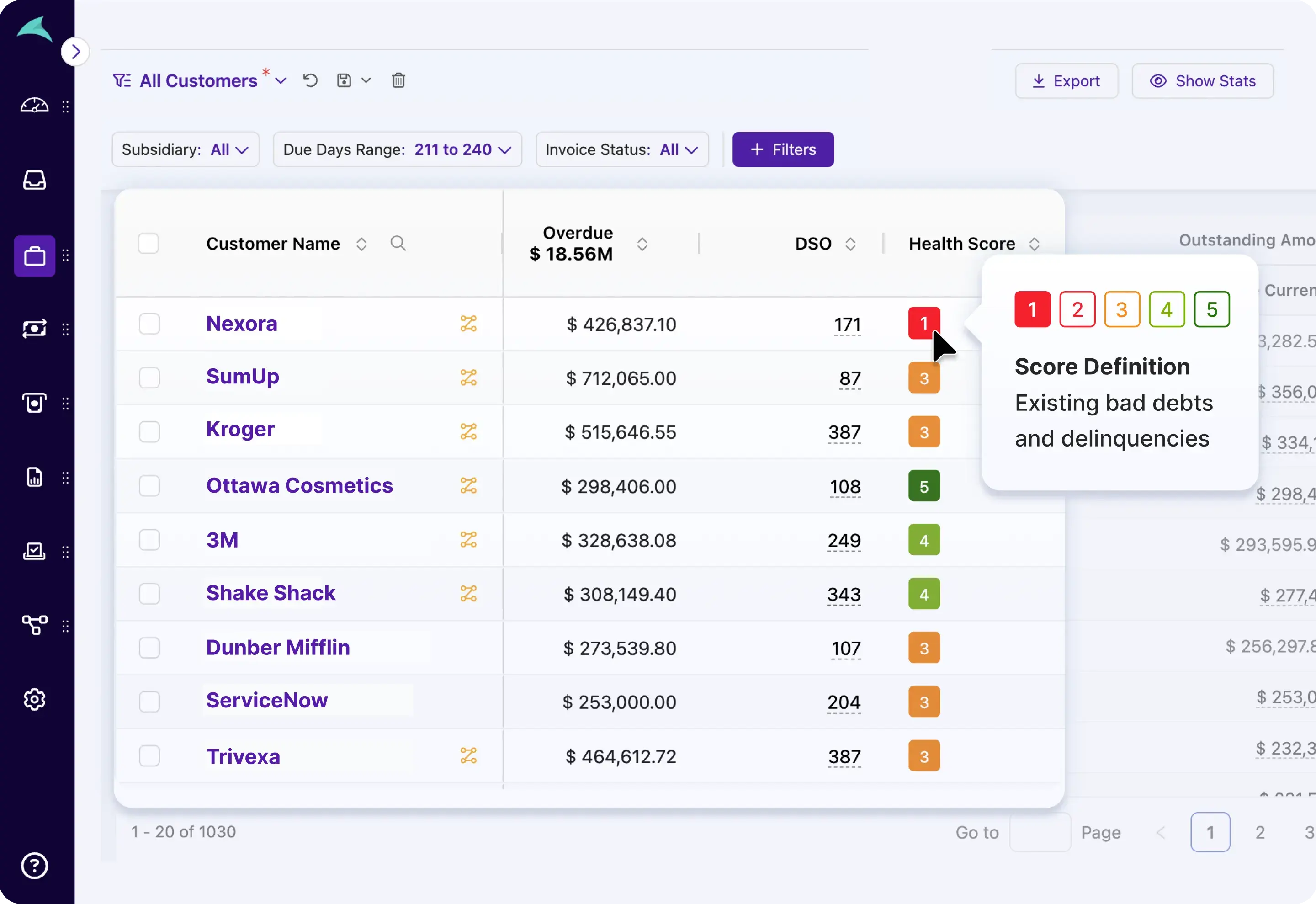

- Which receivables are truly at risk, given recent customer behavior?

- Which balances will convert into cash in the next 7, 30, or 60 days; not just “eventually”?

- Which disputes, deductions, and promises are fragile enough to threaten near-term liquidity or covenant headroom?

Those questions depend on data that doesn’t originate in ERP: partial payments, ambiguous replies, disputes, promises-to-pay that may or may not be honored, portal notifications that contradict what the ledger shows.

Turning those signals into a defensible cash view isn’t a posting problem. It is a judgment and timing problem. When you use ERP as your primary AR decision surface, you anchor AR to the moment a transaction becomes finalized; precisely when the economically interesting part is over.

You did not misconfigure ERP. You misassigned responsibility.

Micro-frustrations indicating that there’s an architecture problem

If you map a week in your AR team’s life, you won’t find many ‘big failures.’ You’ll find a long list of micro-frustrations that, in finance language, add up to drag on cash, Opex, and risk.

Patterns repeat across organizations:

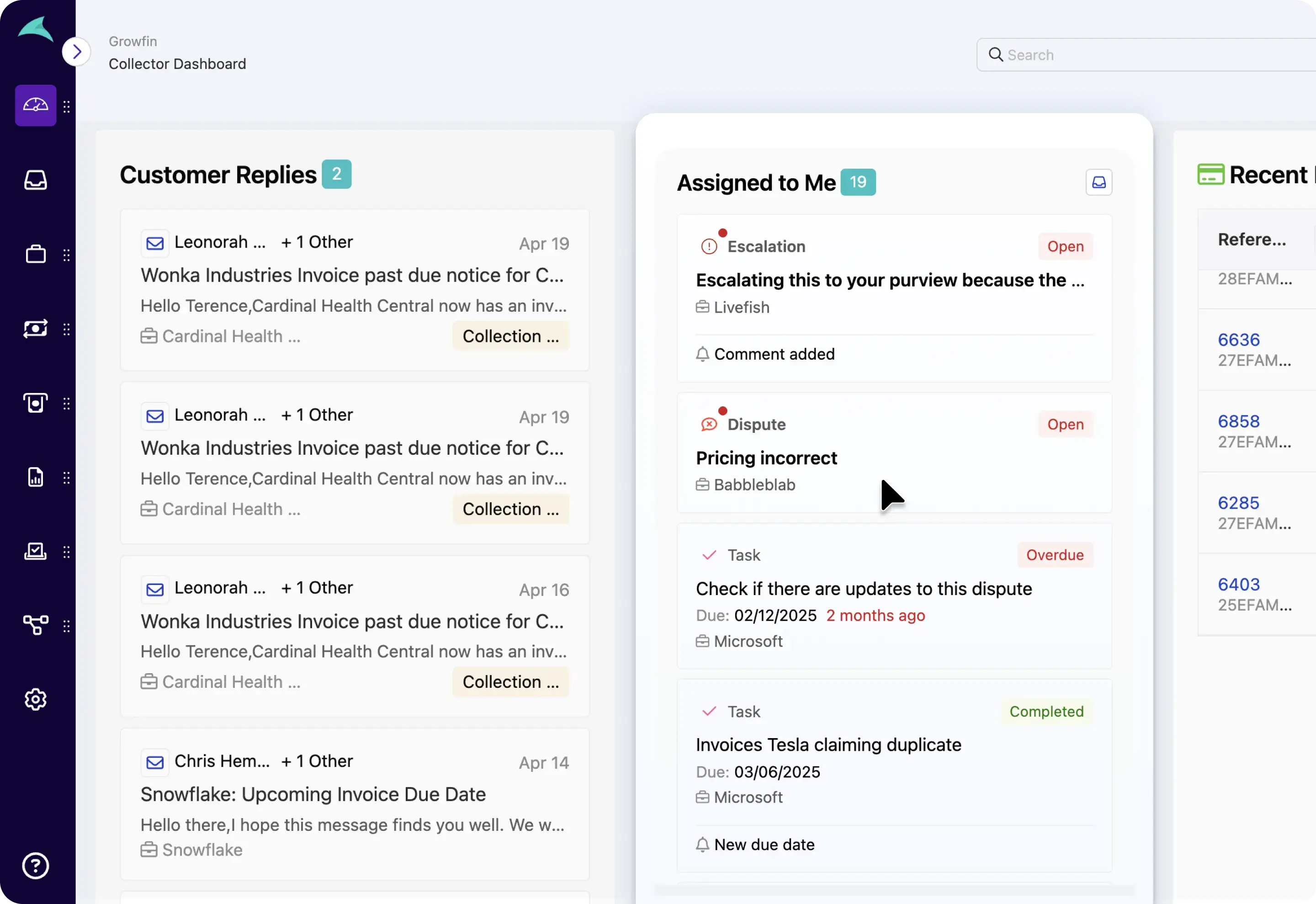

- Signal scattering. Payment confirmations in bank portals, disputes in shared inboxes, short-pay reasons in PDFs, contract nuance in CRM, final postings in ERP. No single surface tells the full story for a given customer.

- Context reconstruction. Before any meaningful customer touch, a collector has to stitch together what actually happened. The first ten minutes of the call are spent re-learning history instead of negotiating outcomes.

- Ownership diffusion. Items bounce between AR, Sales, Customer Success, and Operations with no single, system-visible owner or SLA.

- Decision amnesia. Concessions are agreed in email and never captured as structured data, so the same edge cases reappear and are argued from scratch.

Individually these feel “annoying but manageable.” Together they:

- Flatten AR operating leverage: additional headcount doesn’t translate into proportional improvements in DSO or bad-debt.

- Increase earnings volatility: small, opaque exceptions accumulate into quarter-end surprises.

- Consume expensive talent on workarounds rather than on strategy and risk management.

You can try to fix each frustration with another process tweak. Or you can acknowledge the root cause: you’re running a real-time, interpretive function across tools that were built for static record-keeping.

How these frustrations hit P&L and working capital

ERP-centric AR architectures destroy value. Hence, that means each of the micro-frustrations need to be translated to how it impacts P&L, and working capital for finance leaders.

- Working Capital and the Cost of Slippage

Trapped working capital ≈ (Annual credit revenue ÷ 365) × effective DSO

Every structural source of delay such as unapplied cash, slow dispute cycles, weak prioritisation, shows up as higher effective DSO; not contractual DSO. The difference is that the cash you’re financing as a direct impact of this is, purely because your AR decisions are working on fragmented information.

ERP can tell you contractual DSO and booked balances. Only an AR intelligence layer can compress effective DSO by analysing payment behaviour, recommend actions, and quietly reduce write-offs.

2. Cost of Misallocated Collector Time

Return on collector time ≈ Δ(Expected cash) over a period ÷ Collector hours deployed

In an ERP-first model, worklists are driven by aging, high-effort accounts that would have paid anyway absorb attention, and fragile, risky accounts are discovered late.

You get the same labour cost with lower-risk adjusted cash impact. An AR tool that treats cash-at-risk with the highest priority, can show you account by account, how re-prioritisation changes ROIC/AR headcount

3. Cost of Unexplainable Exceptions

Every time a dispute ends in a write-off or concession, there is an implicit capital charge:

- Operational risk: "What’s the pattern behind these exceptions?"

- Model risk: "None of our forecasts for all our customer segments are accurate. Why?"

- Relationship risk: “This is dangerous, we are training our customers to expect write-offs and discounts”

There is a simple test to see if these costs are relevant for you:

- How many material AR exceptions can you explain, in system data, without reconstructing email threads?

- How many themes can you see without someone building a one-off analysis in Excel?

ERP, on its own, will never answer those questions. An AR intelligence layer can; if you treat “decision lineage” as a first-class requirement, not an afterthought.

So what is an AR intelligence layer in practice?

An AR intelligence layer is not ‘AR in a nicer UI’, but a completely different operating layer, that at the minimum should:

- Drive decisions using data which ERP can’t see in real-time: inbox traffic, portal status, remittance PDFs, call outcomes, CRM context

- Have a single golden record of truth for each customer: including invoices, disputes, promises, risk signals, and ownership

- Have real-time prioritisation: based on cash-at-risk, customer and payment behaviour

- Contain briefs on decisions: capturing why a concession, escalation, or write-off was made, and by whom

From the vantage point of an ERP, nothing changes: it still receives invoices, cash, adjustments.

From the vantage point of the AR team, everything changes: it measures customer risk, segments customers, tailors follow-ups, automatically matches and posts payments using AI, captures remittances automatically, and much more.

Three domains where ERPs should hand-off to AR

AR intelligence for Collections:

- Detection of behavioural shifts (silence after P2P, recurring disputes, change in payment cadence, etc)

- Re-prioritize accounts based on cash-at-risk, and expected impact on the cash curve if you act this week.

- Orchestrate touchpoints across preferred channels with a single narrative per customer.

When AR intelligence comes into the picture, the difference would be that your collections are managing a risk portfolio, rather than a queue.

AR intelligence for disputes and deductions:

- Treating disputes with defined ownership, SLAs, internal collaboration, and root-cause tagging.

- Preserve decision rationale and audit trail to ensure future concessions are biased and are consistent and defensible.

- Use root-cause analysis to bring into effect structural fixes in pricing, billing, and service.

When AR intelligence comes into the picture, the difference would be differentiating between common and isolated fixes, while ensuring unbiased, personalized solutioning, in an automated manner.

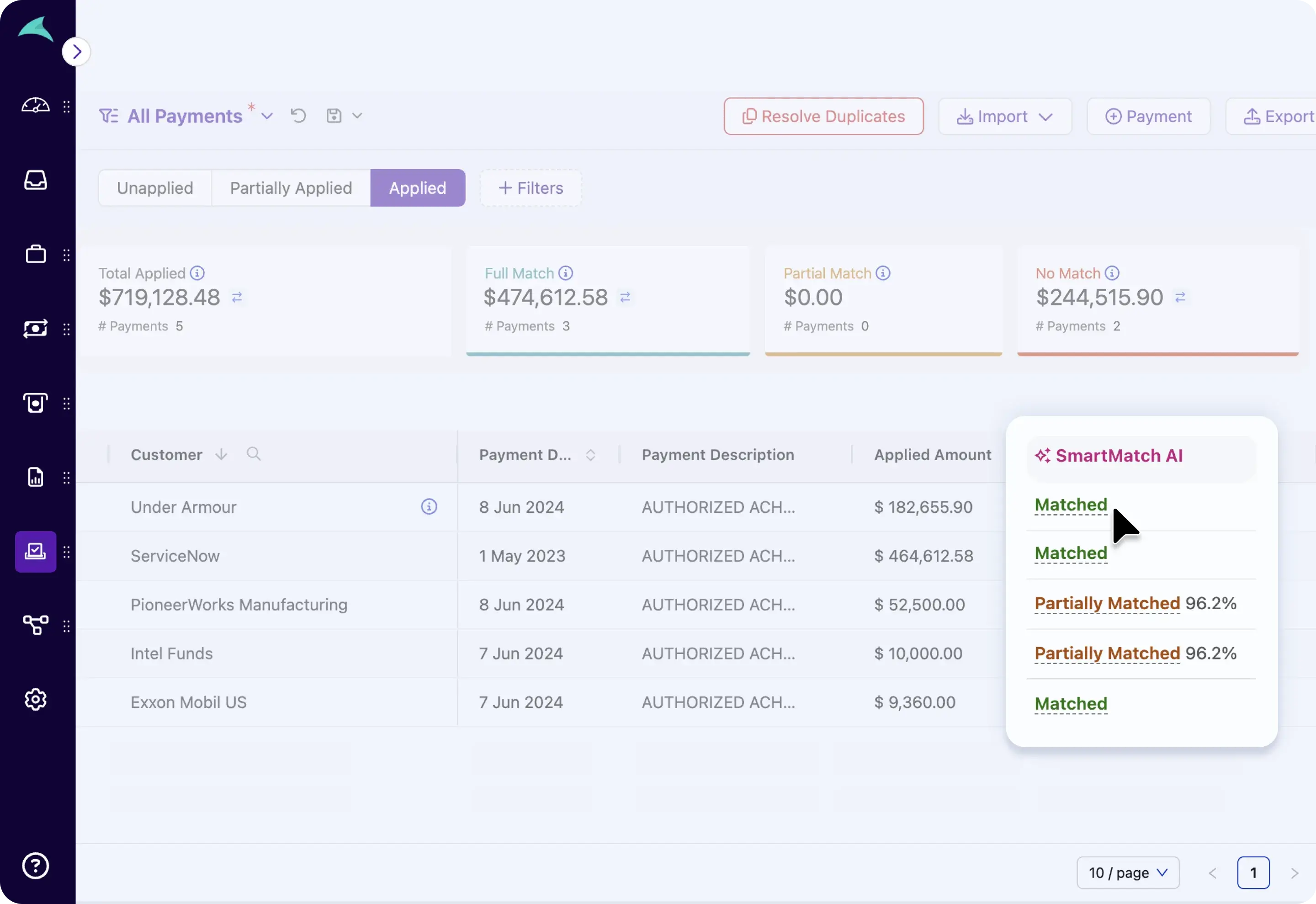

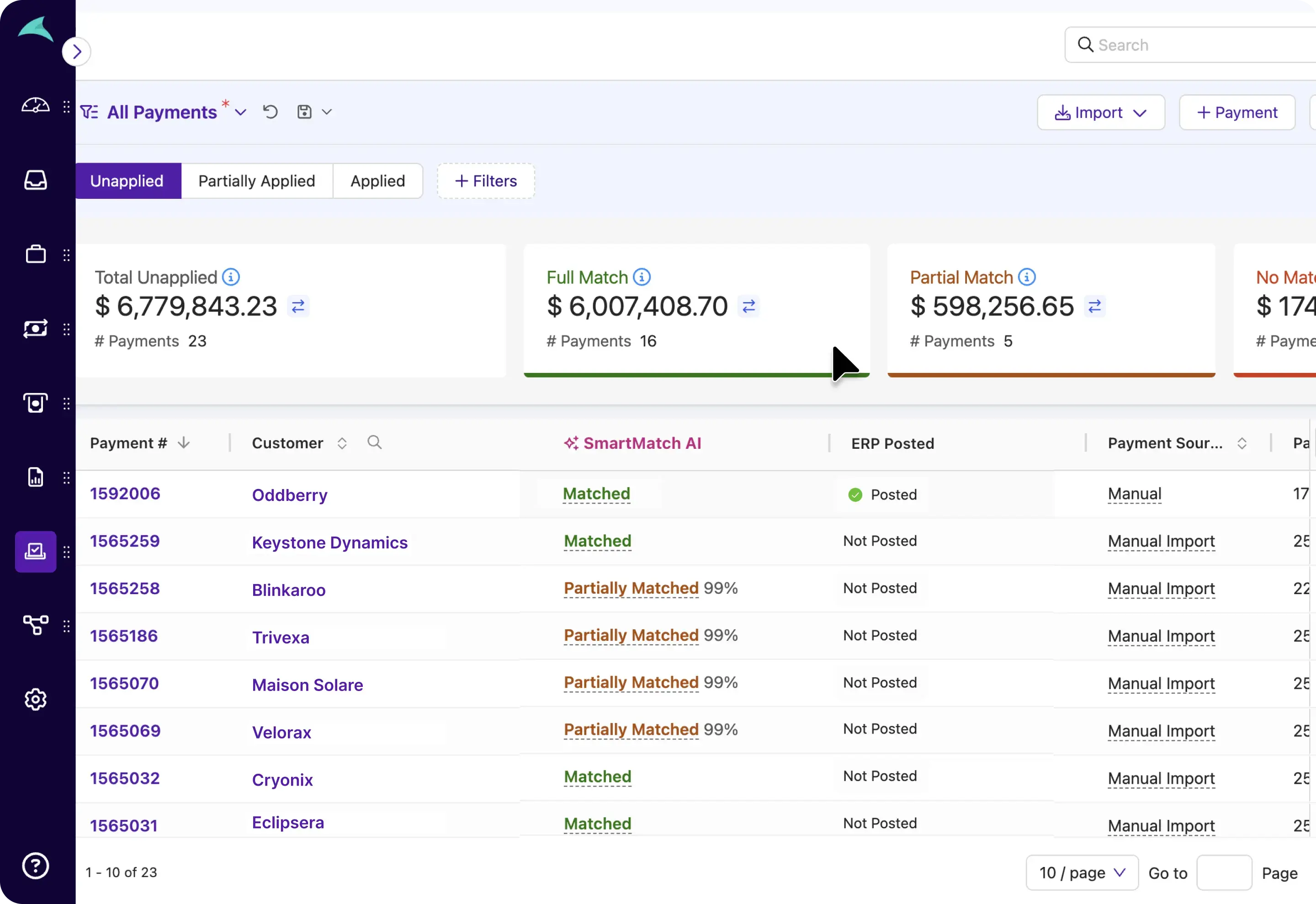

AR Intelligence for Cash Application:

- Read remittance details across emails, files, lockbox, etc.

- Propose matches with confidence scoring, based on patterns, and references

- Surface only ambiguous exceptions which require human intervention with the necessary context.

When AR intelligence comes into the picture, the difference would be in the amount of working capital that the treasury teams decide to obtain unnecessarily.

The question that cannot be ducked under anymore

If you’ve lived through an ERP experience, you already know this: you don’t really run AR inside your ERPs. You run it around your ERP; in inboxes, spreadsheets, chat history; and then backfill the ledger.

The only real question is whether you want to: keep treating that reality as a process flaw and tolerate the monetary drag, or design an AR intelligence layer that lets ERPs be exactly what it's brilliant at without muddying the perception of AR within the organization.

.webp)

.webp)

.webp)

.webp)