.png)

.webp)

.webp)

.webp)

.webp)

Sarah pulls up three different spreadsheets, checks her email for payment confirmations, then realizes she called the same customer twice yesterday. What does Sarah need?

Accounts receivable automation.

Strap in for the ride. As one of the leading accounts receivable automation platforms, we understand the nitty gritties of it. This guide will take you through the basics of ar automation, its impact and ROI, features you should look out for, comparison of the technologies available, and an implementation road map to put you on the fast track towards automating your accounts receivable process.

What is accounts receivable automation?

Accounts receivable (AR) automation is the practice of using software to handle the repetitive, error-prone work across the invoice-to-cash cycle: generating and delivering invoices, sending scheduled reminders, accepting digital payments, matching and applying cash, reconciling accounts, managing disputes, and surfacing real-time reporting.

It replaces manual, spreadsheet-driven processes with system-guided workflows so teams can focus on exceptions, customer relationships, and strategic initiatives.

When accounts receivable teams rely on spreadsheets, email inboxes, and memory alone, cash slows down and small mistakes compound into major delays. 86% of businesses report up to 30% of monthly invoiced sales are overdue, while 81% say it takes 1-4 contacts to collect on a single overdue invoice. Perhaps most telling, 27% of finance teams spend at least half their time resolving invoice disputes rather than strategic work.

The objective behind automation accounts receivable is to collect faster, predictably, and efficiently.

How accounts receivable automation works

There are four key areas that AR automation targets:

- Invoice & delivery: ERP issues the invoice; the AR system adds the right backup (PO/POD/timesheets), chooses the customer’s channel (email, portal, EDI), and tracks send, open, download, or rejection so “we never got it” is easy to disprove. Quick primer: the accounts receivable process.

- Risk-aware follow-up: Behavior-based sequences start as soon as delivery is confirmed. High-risk accounts get tighter cadences and earlier escalation; strategic accounts get context-rich nudges. Sequences pause on a promise-to-pay or dispute and resume if deadlines slip. See the AR collections playbook.

- Payment: Every invoice carries a pay link. The system surfaces the customer’s preferred rail (ACH, RTP, card) and posts confirmations in real time so dunning stops the moment funds arrive. More fundamentals in AR automation basics.

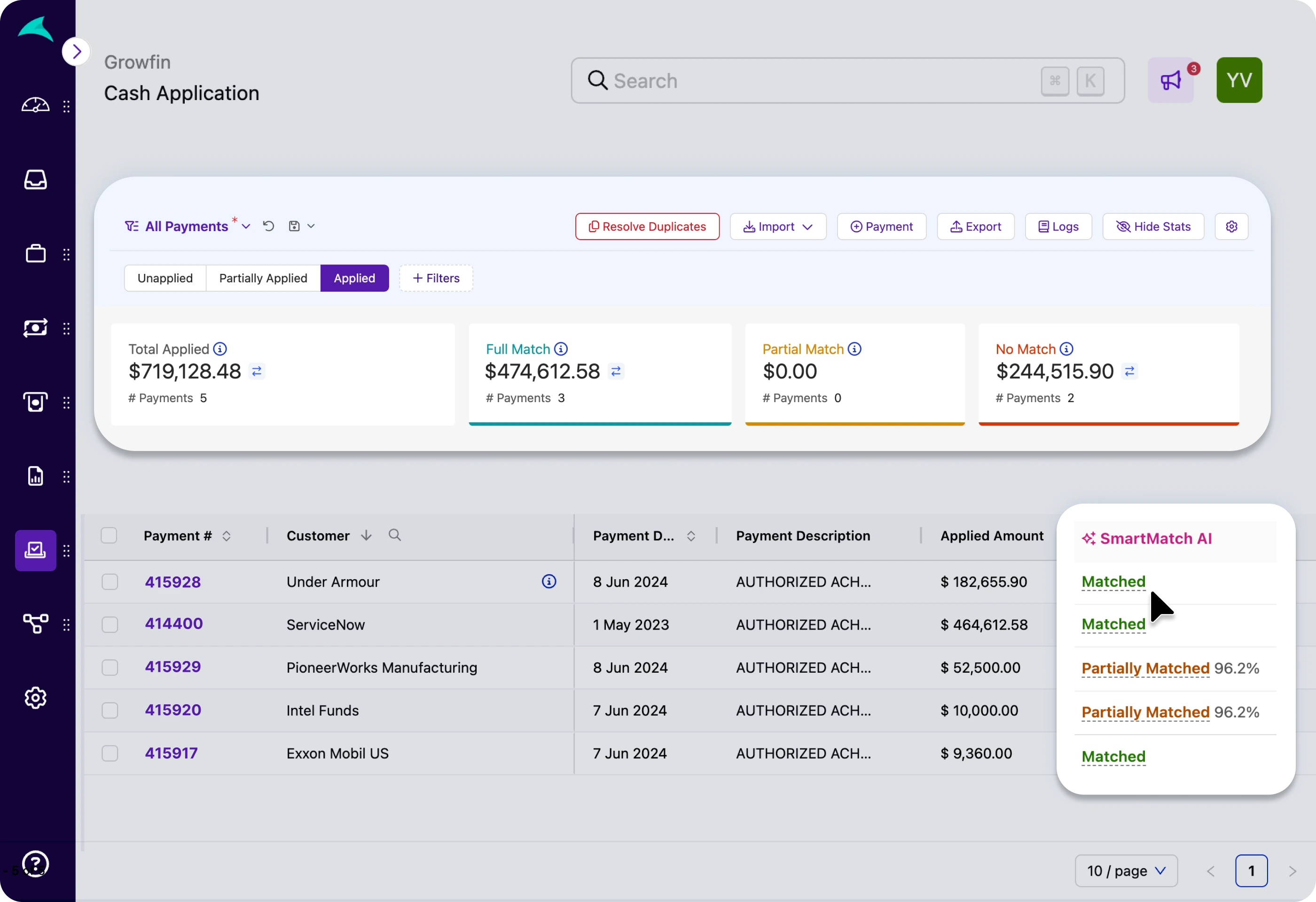

- Cash application: Bank feeds, lockbox files, and remittance emails land in one queue. Matching runs in three passes—deterministic, rules, then ML—with short-pays auto-coded and clean items auto-posted to the ERP with an audit trail.

- Forecast & alerts: Predicted pay dates roll up from invoice to customer to entity. Alerts fire on missed promises, dispute spikes, or unusual silence, helping finance catch slippage early. For patterns and tactics, see how top companies predict payment delays.

The biggest challenges in accounts receivable processes today

Visibility gaps beyond totals:

A single aging number hides the truth. CFOs need entity, region, collector, and customer-tier views, with drill-downs by dispute type and promise-to-pay reliability. Accounts receivable automation standardizes definitions and pipes live data into one canvas so reporting stops being a weekly export party. Good companion read: real-time AR analytics for CFOs.

Payment unpredictability:

The math isn’t just DSO. It’s consistency. Which customers slip after quarter-end, who pays on the second reminder, who never honors a PTP. Seasonality, approval stacks on the AP side, and portal stalls all bend the curve. Predictive signals and behavior-based cadences are what bend it back. Lay the groundwork with DSO is not the whole story and the piece on predicting payment delays.

Dispute drag and unclear ownership:

Evidence sits in inboxes, file shares, and someone’s memory. Each missing attachment adds days. Accounts receivable automation creates a single dispute record with reason codes, SLAs, and threaded documents so finance, sales, operations, and the customer work from the same facts. If you need a primer, point to the explainer on AR disputes and protecting relationships.

Multi-entity, multi-currency, multi-tax reality:

Subsidiaries, different ERPs, local tax rules, and e-invoicing mandates strain manual controls. Data must reconcile at the group level without breaking local requirements. Automation enforces data standards on ingest, tracks intercompany offsets, and keeps reporting apples to apples. For the operational angle, see accounts receivable management and scaling guidance in navigating AR growth.

Cost-to-collect:

Every extra touch and rework hour eats return. Lockbox fees. Portal re-keying. Ad hoc dunning. Collector time spent finding the right person instead of resolving the issue. Accounts receivable automation cuts touches with smarter prioritization and clean handoffs, then proves it in a dashboard you can defend at the ops review. Useful context: why manual AR costs more than you think and industry examples like supply chain collection costs.

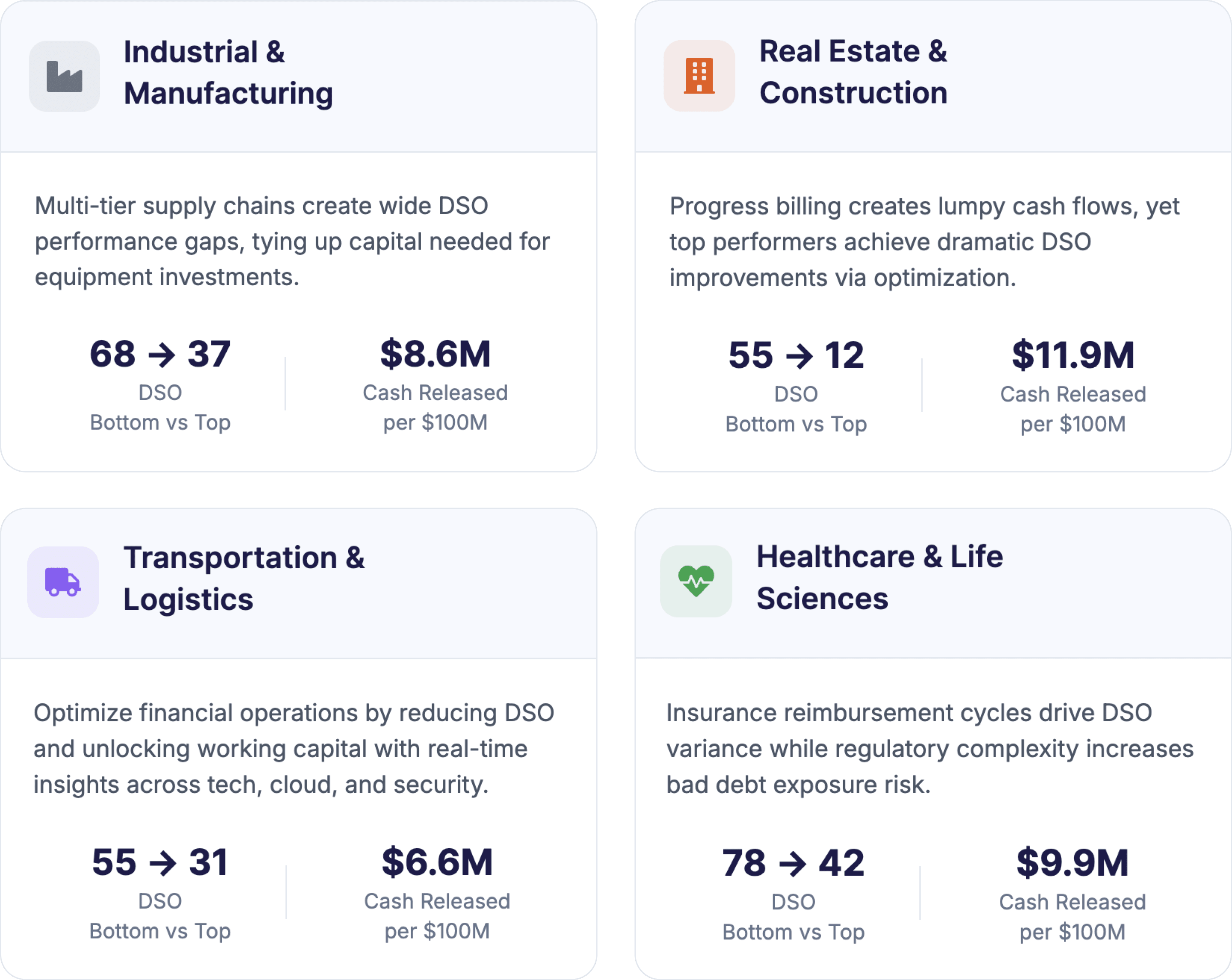

The working capital impact of DSO by industry

Overdue receivables represent trapped cash that could otherwise fund operations or growth. The 2025 DSO & Working Capital Benchmark quantifies the working capital improvement that comes with moving from median to top-quartile DSO benchmarks based on 1200+ 10-K reports.

Mid-market firms ($200M–$1B revenue) face the widest variance in DSO performance because they've outgrown manual processes but haven't yet industrialized their AR operations. That said, bear in mind that DSO is not the whole story.

The business case for automating accounts receivable

Automation transforms receivables from a reactive cost center into a predictable cash engine. Here are the four key benefits any CFO would appreciate.

Faster cash collection & lower DSO

This is the most straightforward benefit: automation removes wait time between invoice events and follow-ups while making prioritization data-driven rather than reactive.

- Air Comm: 33% DSO reduction, 22% fewer past-due invoices, 30% improvement in average days late, 20% reduction in overdue dollars

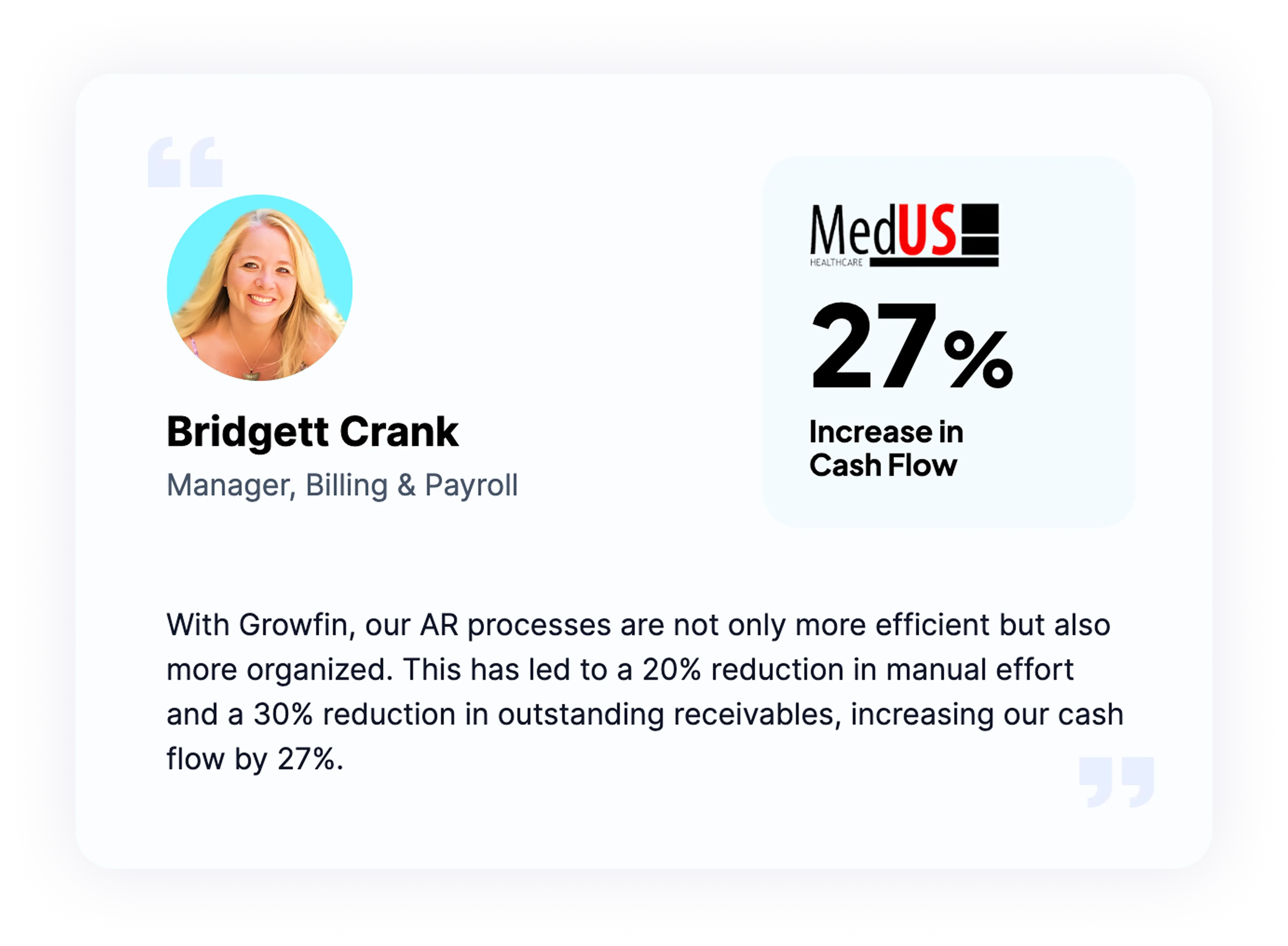

- MedUS Healthcare: 27% increase in cash flow alongside 30% reduction in outstanding receivables

.webp)

Teams commonly see 25-40% DSO improvements by switching to automated accounts receivable.

Measurable productivity gains

Accounts receivable automation reduces time spent on clerical tasks and that productivity translates directly into the ability to scale receivables without proportional headcount increases—or redeploy existing team capacity toward strategic work.

- MedUS Healthcare cut manual effort by 20% while resolving disputes faster through centralized documentation

- Typical productivity improvements: 40-60% reduction in time spent on routine AR tasks

- Cost-to-collect reduction: Lower operational costs per dollar collected through systematic workflows

Turns out manual AR is more expensive than you think.

Error reduction & faster dispute resolution

Manual proceses in accounts receivable management introduces preventable mistakes that trigger disputes and delay cash. The most common friction points include:

- Data entry errors during invoice creation

- Missing documentation during dispute resolution

- Misapplied payments due to unclear remittance data

- Communication gaps between AR, Sales, and Customer Success teams

Enterprises report 60-80% reduction in billing-related disputes and 50% faster resolution times when documentation and communication are centralized.

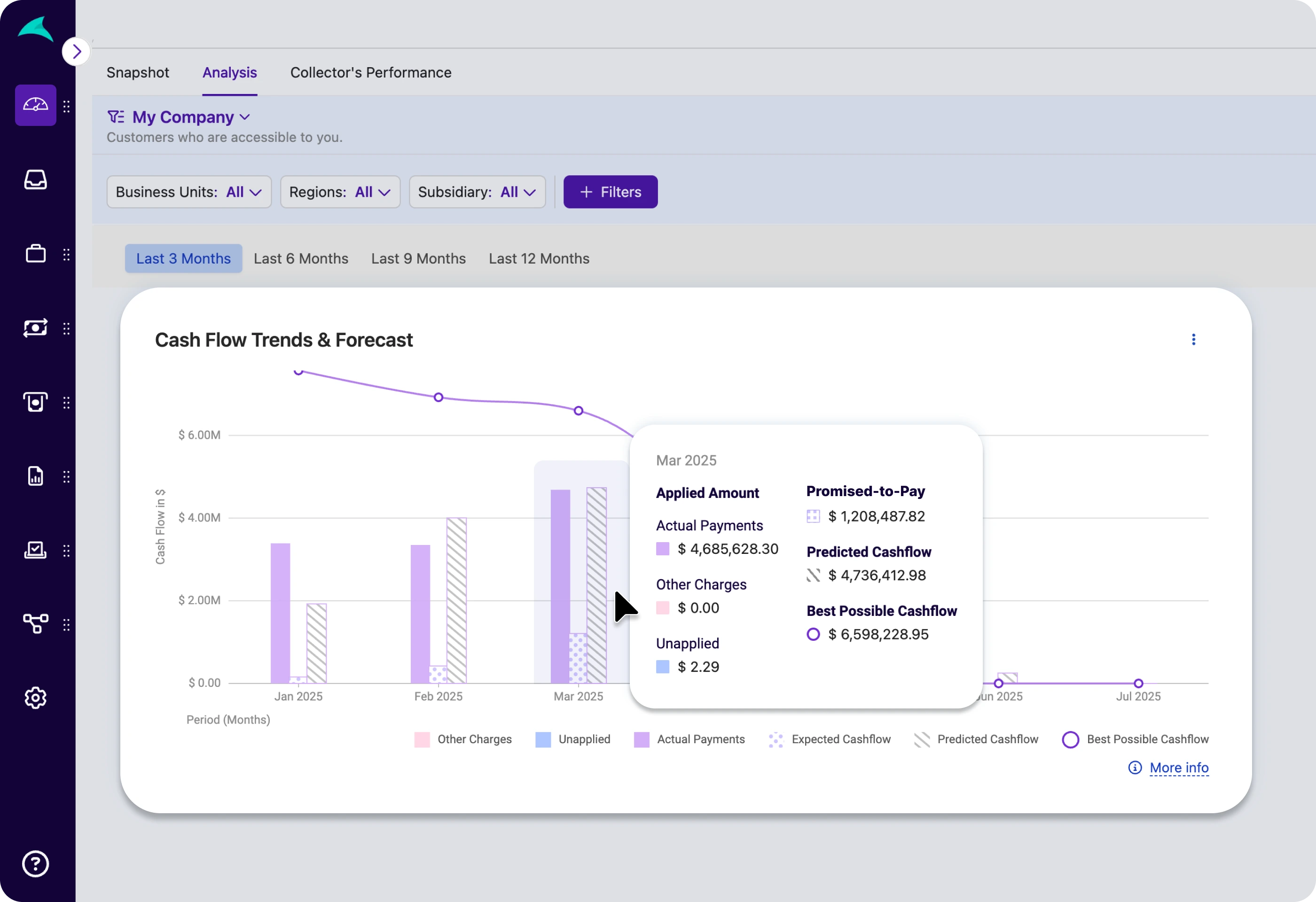

Enhanced cash flow forecasting

When predicted pay dates roll up by customer and invoice, cash forecasts stop being guesswork. Modern AR platforms provide:

- Expected vs. predicted vs. best-case scenarios based on historical payment behavior

- Confidence intervals around each prediction

- Early warning signals when customers show signs of payment delay

Bottom-line impact: CFOs gain 2-4 weeks additional visibility into cash positioning, enabling better working capital decisions.

Quick ROI calculation framework

Check out where you stand against peer-groups with the 2025 DSO benchmarks and working capital calculator. You need just three inputs to quantify accounts receivable automation benefits:

1. Working capital released from DSO Gains

Daily sales × days of DSO reduced = Cash released

Example: $100M revenue, 5-day DSO improvement = $1.37M released

2. Labor savings

Hours saved per month × fully loaded rate × team size = Cost reduction

Example: 20% effort reduction on 3-person team = $180K annually

3. Credit losses avoided

Current write-offs × improvement rate = Bad debt reduction

Example: $1M write-offs × 20% improvement = $200K recovery

Typical payback: Most teams see ROI within 3-6 months, then compound benefits as automation coverage expands. Here's more on going from manual to modern AR.

Features of a modern accounts receivables automation software

A comprehensive accounts receivable automation platform should address the entire invoice-to-cash process plus the underlying data and collaboration infrastructure. Here's a quick list of features you should look out for from future-proof accounts receivable automation softwares:

1. Invoicing & Delivery

- Multi-format invoicing: PDF and machine-readable formats with automated PO/contract/usage data attachment

- Multi-channel delivery: Email tracking, customer portal downloads, EDI transmission

- Late fee automation: Rules-based application with customer notification

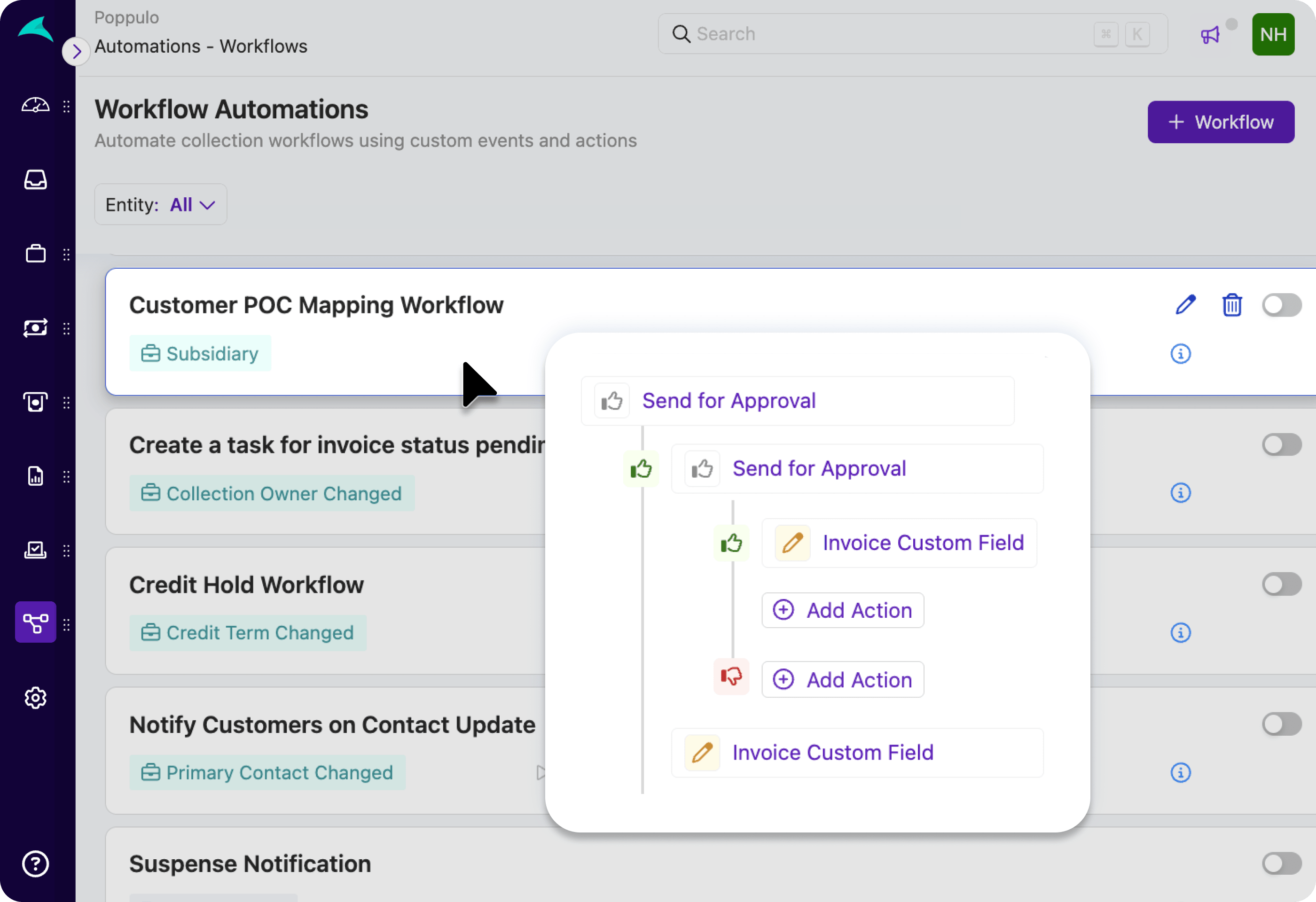

2. Collections & Dunning

- Personalized dunning workflows: Invoice and statement-level sequences that auto-start/stop based on payment status, disputes, or promises-to-pay

- AI-powered prioritization: Risk scoring and aging analysis to surface next-best accounts for collector attention

- Integrated communication: One-click statements, logged call notes, CRM sync for Sales/CS visibility

- Promise-to-pay tracking: Automated follow-up on commitments with reliability scoring

.webp)

Read the ultimate playbook of collections strategy.

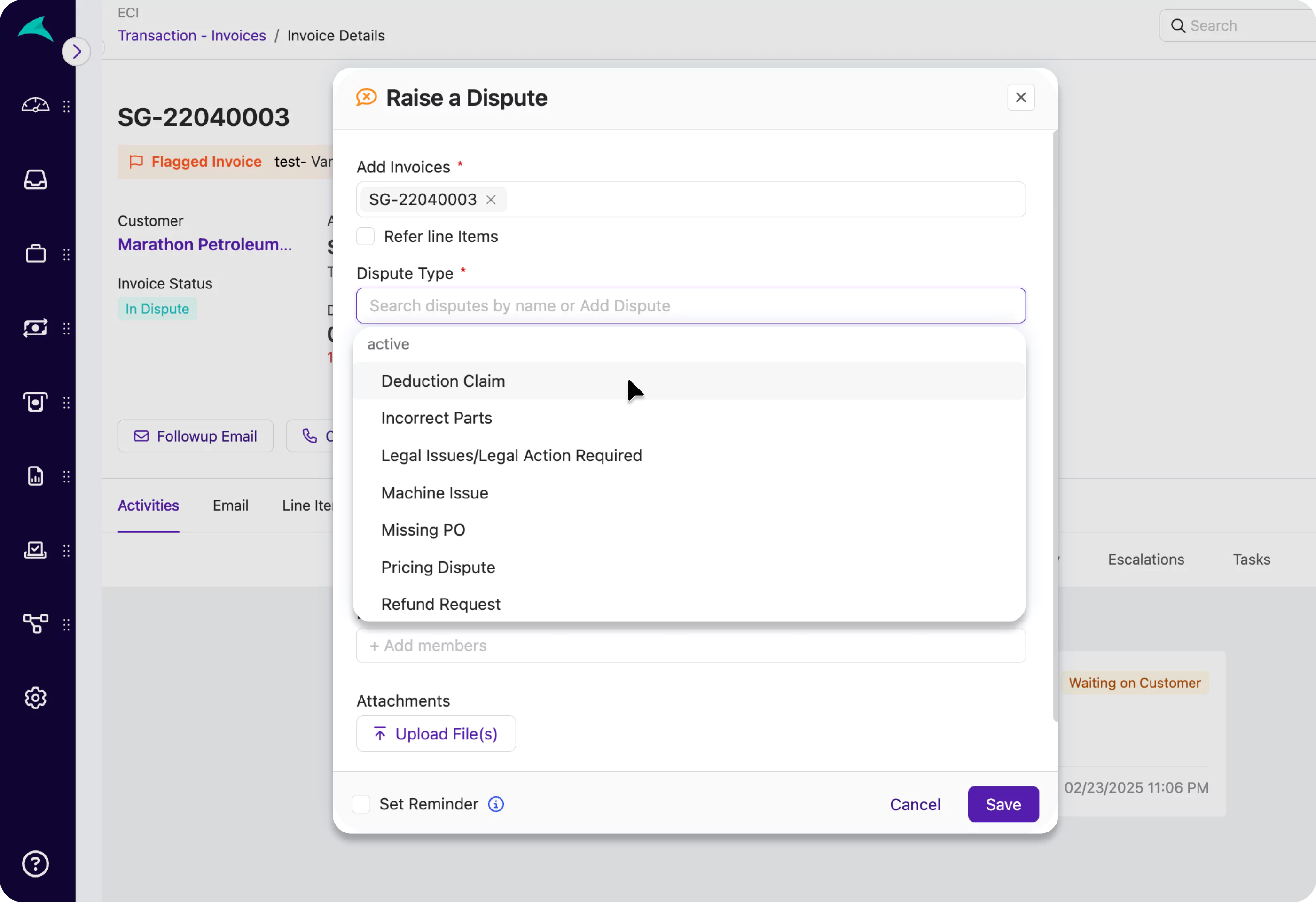

3. Disputes & Deductions Management

- Self-service dispute portal: Customer-initiated disputes with reason codes, evidence upload, and SLA timers

- Cross-team collaboration: Automated routing to Sales/Operations with @mentions and approval workflows (read more on sales-finance collaboration for collections)

- Root-cause analytics: Dispute categorization feeding continuous improvement in billing and operations

- Audit trail preservation: Complete documentation for credit memos and write-offs

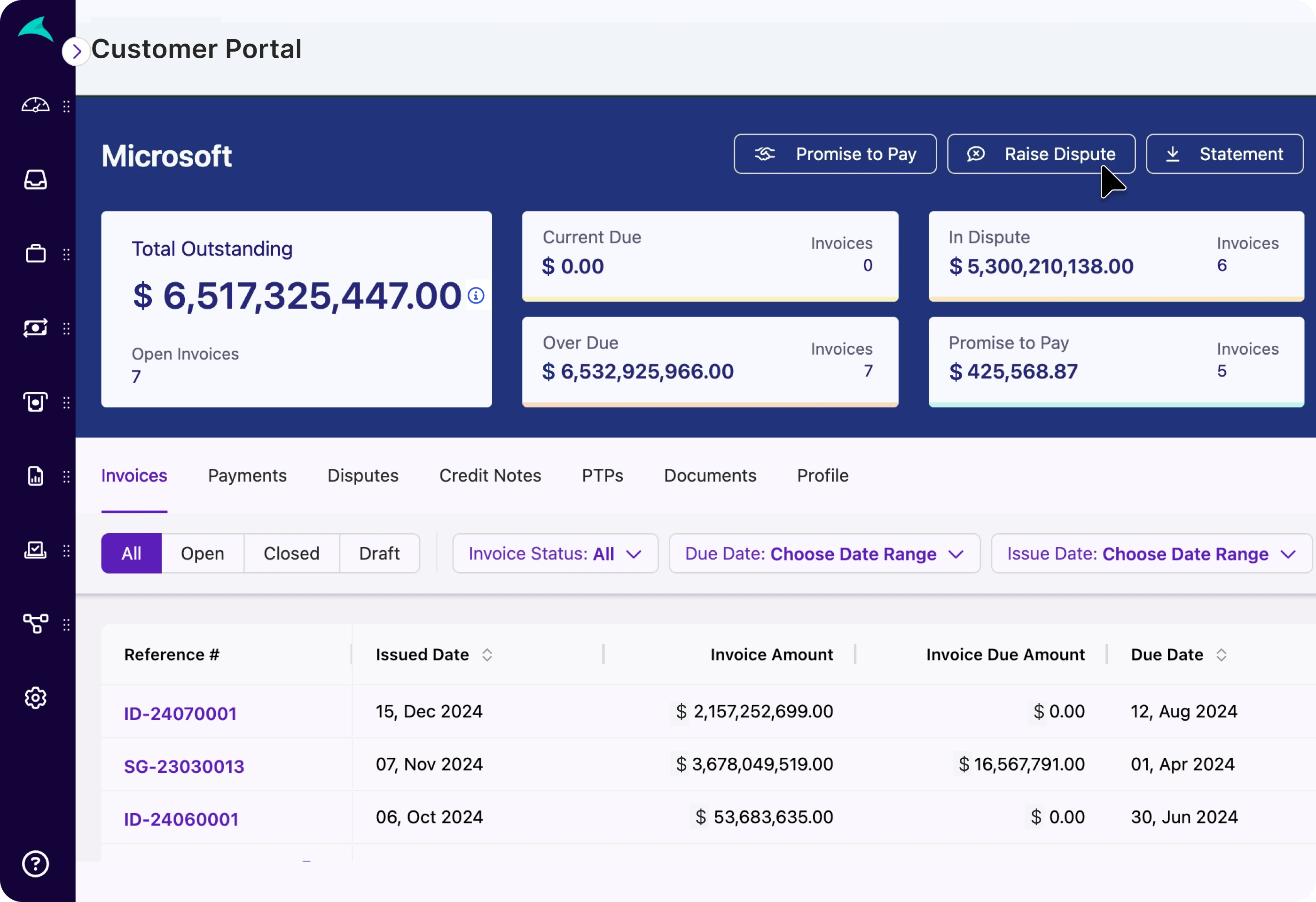

4. Customer Experience & Self-Service

- Branded customer portal: Statement access, dispute submission, PTP management, document downloads (read: preserving customer relationships in AR)

- Embedded payment links: Integration with preferred payment methods with real-time AR sync

- Communication preferences: Channel selection (email, portal, phone) by customer

- Account transparency: Real-time balance and payment history visibility

5. Cash Application & Reconciliation

- Multi-source remittance capture: OCR and parsing for banks, lockbox, email attachments (BAI, BAI2, MT940, EDI/IDX, CSV, PDF)

- AI-powered matching: Three-tier logic from deterministic rules to ML-based suggestions with confidence scoring

- Exception handling: Automated duplicate detection, adjustment processing (discounts, taxes, FX), query resolution

- Same-day posting: Automated ERP updates with configurable thresholds and comprehensive audit trails

Benchmark Expectations:

- 98% payment extraction accuracy

- 80%+ precise invoice matching

- 80%+ same-day posting rates

6. Forecasting & Risk Management

- Predictive cash modeling: Bottom-up forecasts from invoice-level predicted pay dates (read: how top companies predict payment delays)

- Scenario planning: Expected, best-case, and likely collection outcomes

- Explainable predictions: Transparent factors (aging, customer history, dispute flags, communication patterns)

- Early warning systems: Risk scoring for payment delays and customer health deterioration

7. Analytics & Reporting

- Real-time AR dashboards: Aging, DSO, CEI, collector productivity, dispute metrics (read: Why real-time accounts receivable is the new CFO standard)

- Multi-entity reporting: Region, business unit, and subsidiary roll-ups with drill-down capability

- Custom report builder: Self-service analytics with scheduled delivery

- Collectors' performance management: understand team performance against targets and expectations

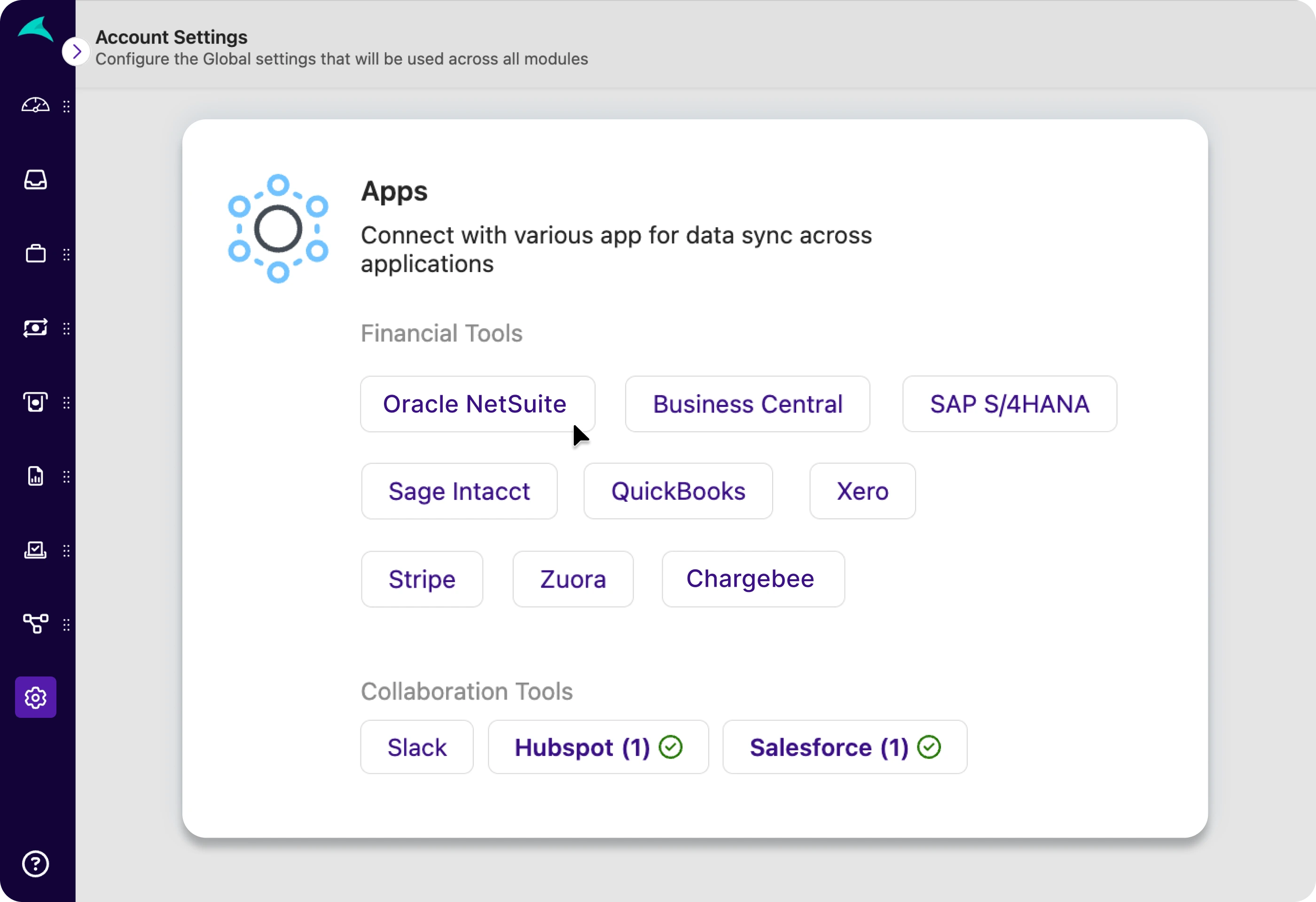

8. Integrations & Data Management

- Bi-directional ERP sync: Real-time invoice, payment, credit memo, and contact updates

- CRM integration: Salesforce/HubSpot sync for account context and task management

- Collaboration tools: Slack/Teams notifications for escalations and approvals (read more: Collaboration is a game changer)

- Bank connectivity: Direct feeds and lockbox integration for straight-through processing

9. Workflow & Governance

- Role-based permissions: Configurable access controls across collections, disputes, cash application

- Approval workflows: Credit, write-off, and settlement approvals with routing logic

- Audit trails: Complete activity logs for compliance and process improvement

- Change management: Training modules and process documentation

Top 12 AR tasks you can automate today

Invoice sending and statements:

Turn time-to-first-touch into same day. Send the right template, in the right format, with the right attachments, and log delivery outcomes. Customer statements generate on schedule or on demand, personalized by account. Backgrounder: accounts receivable process.

Reminder cadences (dunning):

Cadences adapt to behavior. If a customer replies, pause. If a partial hits, switch tone and ask for remittance. If silence continues, escalate internally with context. This is where moving from reactive to proactive pays off; see the collections playbook and proactive AR.

Promise-to-pay tracking:

Log PTPs with dates and amounts. The system watches them and follows up the moment they are missed. Reliability scores roll into risk so forecasts stay honest.

Short-pay handling:

Detect deductions, fees, and discounts on import. Suggest codes, route to the right approver, and post with notes so the account history stays clean for the next touch.

Dispute logging and resolution:

Give customers a simple way to raise disputes with reason codes and evidence. Internally, every dispute gets an owner, SLA, and a checklist that mirrors how your teams actually resolve issues. See the dispute explainer: preserving customer relationships.

Cash application matching:

Run deterministic matches first, then rules, then model suggestions with confidence. Exceptions stay tight and actionable. This is where check-heavy flows in healthcare and supply chain benefit most; tie back to the vertical posts on traditional payments in healthcare and in supply chain.

Auto-posting to the ERP:

When a payment is clean, post it. When it is not, hold it with a reason. Thresholds and audit logs keep auditors comfortable and month-end calm.

Collector worklists:

Every morning starts with a ranked list that factors value at risk, likelihood to pay, aging, relationship context, and today’s SLA timers. Not just alphabet or oldest first.

Renewal and usage nudges for SaaS:

Pre-due reminders include plan context, open invoices, and a pay link. If a card on file is about to fail, nudge early with an update link so revenue doesn’t churn into AR.

Credit and limit controls:

Monitor exposure by account and parent. Alert on over-limit orders or apply a hold when risk spikes. Re-open automatically when a payment clears or a dispute resolves.

Executive dashboards:

Live CEI, DSO, ADD, forecast variance, and collector productivity in one view. Drill to the invoice and see the communication thread. Good framing for this is the real-time AR analytics article.

Export and evidence packs:

One click compiles invoice PDFs, delivery proofs, comms history, dispute notes, and approval trails for audits or escalations. Legal and sales get the same bundle, so the story stays straight.

Buyer guide to compare accounts receivable automation software

When evaluating accounts receivable software, look at capability depth first. Integration quality matters more than most realize. Then there's the AI factor...

Growfin looks at AR software completeness across four levels:

Axis 1: Capability depth

- Collections automation: Dunning sequences, prioritization, communication tools

- Cash application: Remittance parsing, matching logic, posting automation

- Dispute management: Portal, workflows, root-cause analytics

- Forecasting: Predictive modeling, scenario planning, confidence scoring

Axis 2: Integration & data

- ERP connectivity: Bi-directional sync quality and real-time capabilities

- Banking integration: Lockbox, file formats, API connectivity

- Third-party ecosystem: CRM, communication tools, reporting platforms

- Data quality: Master data management, deduplication, enrichment

Axis 3: AI & controls

- Machine learning maturity: Prediction accuracy, model explainability, continuous learning

- Automation guardrails: Confidence thresholds, exception handling, approval workflows

- Decision transparency: Audit trails, model interpretability, business rule visibility

- Risk management: Fraud detection, compliance monitoring, control frameworks

Axis 4: Operating model fit

- Implementation approach: Vendor-led vs. self-service configuration

- Change management: Training, adoption support, process consulting

- Scalability: Multi-entity, international, high-volume transaction support

- Support model: Response times, expertise levels, escalation paths

Compare top accounts receivable automation softwares

There are more than 10 reasonably good accounts receivable softwares available today. But they are not no-brainer alternatives to each other. Product capabilities, user experience and their future road map would have to be aligned with your monetization model and complexity of operations.

Get a deeper head-to-head comparison of the top 10 accounts receivable automation softwares.

Red flags to watch For

During vendor demos:

⚠️ Black box AI: Can't explain why a payment date is predicted or account is prioritized

⚠️ Integration theater: Demo shows "real-time" sync but implementation requires batch processing

⚠️ Feature inflation: Long lists of capabilities without clear business impact

⚠️ One-size-fits-all: No discussion of industry-specific workflows or compliance requirements

During contract negotiations:

⚠️ Implementation uncertainty: Vague timelines or significant consulting fees beyond software cost

⚠️ Integration gaps: Additional costs for "standard" ERP connections

⚠️ Scalability limits: Per-transaction fees that make growth expensive

⚠️ Vendor lock-in: Difficult data export or proprietary formats

Critical questions to ask your AR software vendor

Capabilities & fit:

- "Show me how you handle our specific dispute types (PO mismatches, pricing disagreements, delivery issues)"

- "What's your auto-posting accuracy for payments like ours (check, ACH, international)?"

- "How do you prioritize accounts when aging, value, and relationship factors conflict?"

Implementation & support:

- "What does 'go-live' mean—automated dunning only, or full cash app and forecasting?"

- "Who configures our workflows—your team, our team, or joint effort?"

- What's your average customer time-to-value for companies our size?"

Technology & integration:

- "Show me a real customer's cash flow forecast—how accurate are your predictions?"

- "What happens when your AI confidence is low—how do exceptions get routed?"

- "How do you handle our ERP's custom fields and non-standard processes?"

Economics & scalability:

- "What's your pricing model as we grow—per user, per transaction, per invoice?"

- "What additional costs should we budget for training, data migration, ongoing support?"

- "How do customers typically expand usage after initial implementation?"

Implementation playbook for accounts receivable automation

Implementing an AR automation software can feel daunting because it replaces so many manual processes and has to work cleanly with your ERP, while ensuring adoption among the team.

Break down your implementation cycle into 3 phases each with their own milestones and metrics to watch out for.

Phase 1: foundation & planning (days 1-15)

Outcome alignment

- Define success metrics: specific DSO targets, productivity gains, forecast accuracy goals

- Set initial scope: prioritize collections + cash app OR collections + disputes (avoid trying to do everything at once)

- Identify weekly KPIs: DSO/ADP, % overdue, CEI, auto-match rates, dispute resolution time

Data & integration planning

- Establish single source of truth for customers, invoices, contacts, payment data

- Standardize master data: payment terms, customer segments, reason codes

- Map required integrations: ERP (bi-directional), banks (lockbox/feeds), CRM (context), collaboration tools (notifications)

Stakeholder preparation

- Identify process owners: collections manager, cash application specialist, dispute coordinator

- Plan change management: communication strategy, training schedule, success measurement

- Set governance framework: approval workflows, escalation paths, exception handling

Phase 2: configuration & testing (days 16-45)

Core workflow setup

- Collections: 2-3 dunning playbooks (high/medium/low risk) with clear start/stop rules and branded templates

- Customer portal: Self-service access for statements, disputes, promise-to-pay submissions

- Disputes: Reason codes, SLA timers, routing logic with required documentation at intake

- Cash application: Remittance sources, matching rules layered from deterministic to AI-assisted

Dashboard & reporting

- Live executive view: aging, CEI, collector activity, dispute status, promise-to-pay reliability

- Forecast modeling: expected/predicted/best-case scenarios with explainable factors

- Exception monitoring: low-confidence matches, disputed invoices, broken promises-to-pay

Pilot execution

- Select clean cohort (e.g., top 150 customers in primary region) for end-to-end testing

- Run parallel processes for 2-3 weeks to validate accuracy and identify gaps

- Hold twice-weekly standups to review auto-match confidence, dispute resolution, and PTP slippage

Phase 3: scale & optimization (days 46-90)

Rollout strategy

- Expand by customer segment or geography based on pilot learnings

- Tighten SLA expectations as team becomes comfortable with new workflows

- Document standard operating procedures and exception handling protocols

Performance monitoring

- Weekly executive readout: CEI trends, DSO/ADP movement, automation coverage, forecast accuracy

- Monthly deep-dive: collector productivity, dispute root causes, customer satisfaction indicators

- Quarterly business review: ROI measurement, expansion opportunities, process optimization

Continuous improvement

- Refine dunning templates based on response rates and customer feedback

- Adjust auto-posting thresholds as confidence in matching accuracy increases

- Expand automation coverage to additional customer segments and transaction types

Success metrics benchmarks

To make sure you stay on track and with purpose, it's useful to assign milestones across the 4 phases of implementation. Here's an example of what that might look like:

Week 4 targets:

- Collections automation: 80% of eligible customers on automated sequences

- Cash application: 70% auto-match rate for standard payment types

- Dispute management: All new disputes routed through standardized workflow

Week 8 targets:

- DSO improvement: 5-10% reduction from baseline

- Productivity gains: 20% reduction in manual effort per collector

- Forecast accuracy: ±15% variance between predicted and actual cash

Week 12 targets:

- Full automation coverage: 95% of invoices in scope

- Auto-posting rate: 80% same-day posting for matched payments

- Team adoption: 100% of activities logged in AR platform vs. external systems

Common implementation pitfalls

As with most things in life, nothing’s perfect. Watch out for common pitfalls that are likely to creep into accounts receivable implementation.

Scope creep

- Problem: Trying to automate everything at once

- Solution: Start with collections OR cash app, then expand after proving value

Data quality issues

- Problem: Poor master data creates matching problems and duplicate customer records

- Solution: Invest 1-2 weeks in data cleanup before system configuration

Change resistance

- Problem: Team continues using old processes (email, spreadsheets) alongside new system

- Solution: Make new system the only way to perform key activities; disable old tools

Premature optimization

- Problem: Spending weeks perfecting dunning templates before testing with customers

- Solution: Deploy "good enough" workflows quickly, then iterate based on real results

Operational use cases of automation in accounts receivable

So you’ve implemented your choice of AR software. Now beyond reducing manual work, what are the use-cases you could expect to handle with the software?

1. Predict and prevent late payments

The challenge: Cash volatility from slow-paying customers and inconsistent follow-up timing.

How automation helps:

- Predictive models flag invoices likely to slip based on customer behavior, aging, and communication patterns

- Prioritized worklists surface highest-risk, highest-value accounts for immediate attention

- Adaptive dunning sequences adjust timing and intensity based on customer responsiveness

Air Comm reduced DSO by 33% and cut overdue dollars by 20% after implementing automated prioritization and sequencing in place of ad-hoc collections processes.

Related Resource: how to encourage on time payments

2. Scale collections without adding headcount

The challenge: Growing invoice volume overwhelming small AR teams with inconsistent follow-up quality.

How automation helps:

- Centralized AR inbox consolidates communications across email, portal, and phone interactions

- Pre-built dunning sequences ensure consistent messaging and timing

- "Next-best action" queues prioritize work by impact rather than chronological order

MedUS Healthcare cut outstanding receivables by 30% and reduced manual effort by 20% by centralizing communications and automating routine follow-ups.

Read: how to improve collections

Industry application:

- SaaS companies: Automated renewal reminders with payment link embedding

- Manufacturing: Trade promotion and PO-specific messaging

- Professional services: Project milestone billing with automated approval routing

3. Resolve disputes without email ping-pong

The challenge: Revenue trapped in "research" status due to scattered documentation and unclear ownership.

How automation helps:

- Customer portal enables self-service dispute submission with evidence upload and reason code selection

- Automated routing directs disputes to appropriate team members (pricing → sales, delivery → operations)

- Shared timeline provides complete conversation history accessible to all stakeholders

MedUS Healthcare reported materially faster dispute resolution after consolidating documentation and communication workflows in a single platform.

Process flow example:

- Customer submits dispute via portal with POD concern

- System auto-routes to operations team with 48-hour SLA

- Operations uploads delivery confirmation and resolution notes

- Customer receives notification with resolution details

- System auto-closes dispute and resumes collections if needed

4. Eliminate unapplied cash bottlenecks

The challenge: Cash trapped as "unapplied" due to unclear remittance data and manual matching processes.

How automation helps:

- OCR and email parsing extract payment details from diverse formats (PDF remittances, bank files, check stubs)

- Three-tier matching logic: exact remittance match → business rules → ML-based suggestions

- Automated posting with confidence thresholds and exception routing for ambiguous cases

Teams typically see 80%+ auto-match rates and same-day posting, contributing to faster month-end close and improved DSO.

Technical implementation:

Tier 1: Deterministic matching on invoice numbers, PO references, exact amounts

Tier 2: Rule-based matching with tolerances for bank fees, early payment discounts

Tier 3: AI-powered matching using customer history, payment patterns, timing analysis

5. Transform AR from back-office to strategic function

The challenge: AR data isolated from sales and customer success, creating blind spots in account management.

How automation helps:

- Real-time CRM sync provides sales teams visibility into payment status and collection activity

- Collaborative workflows enable handoffs between AR, sales, and customer success

- Shared customer timelines eliminate "I didn't know they were having payment issues" scenarios

Higher collector productivity through better account context, plus improved customer relationships through coordinated communication.

Integration examples:

- Salesforce sync: Overdue invoice alerts in account records, automated task creation for account managers

- Slack notifications: Payment confirmations, dispute escalations, promise-to-pay reminders

- Shared dashboards: Customer health scores visible to both finance and sales teams

Industry-specific use-cases of accounts receivable automation

Technology & SaaS

- Focus: Subscription billing complexity, failed payment recovery, international payment handling

- Key metrics: Monthly recurring revenue (MRR) collection rates, payment failure recovery, customer lifetime value impact

- Automation priorities: Payment retry logic, dunning suppression for good customers, churn risk integration

Manufacturing & Distribution

- Focus: Purchase order matching, trade promotion deductions, multi-entity billing

- Key metrics: Deduction resolution time, PO compliance rates, distributor payment velocity

- Automation priorities: PO-aware matching, promotional deduction workflows, territory-based collection strategies

Healthcare & Staffing

- Focus: VMS portal complexity, credentialing documentation, regulatory compliance

- Key metrics: Claims processing speed, compliance documentation completeness, payer-specific DSO

- Automation priorities: VMS-specific dunning, documentation workflow automation, payer relationship management

Professional Services

- Focus: Project-based billing, time approval workflows, client relationship sensitivity

- Key metrics: Project payment completion rates, approval cycle time, client satisfaction scores

- Automation priorities: Milestone-based collections, approval workflow automation, relationship-aware dunning

AI & emerging technologies in AR automation

AI has evolved from experimental to operational in accounts receivable. The most mature implementations use artificial intelligence to predict payment behavior, prioritize collection activities, automate cash application, and provide early warning of potential issues.

Current AI applications in AR

Payment prediction & prioritization Modern AR platforms use machine learning models to rank invoices by likelihood-to-pay and predict payment dates. Key capabilities include:

- Multi-factor analysis: Customer payment history, invoice aging, dispute status, communication responsiveness, seasonal patterns

- Dynamic prioritization: Automated work queues that surface highest-risk, highest-value accounts for collector attention

- Confidence scoring: Transparent probability ranges around predictions with explanations of contributing factors

Business impact: Teams report 25-40% improvement in collection efficiency by focusing effort on accounts most likely to respond positively.

Intelligent cash application AI-powered cash application operates on a three-tier logic model:

- Tier 1 (Deterministic): Exact matching on invoice numbers, PO references, amounts

- Tier 2 (Rules-based): Business logic for partial payments, early payment discounts, currency adjustments

- Tier 3 (ML-powered): Pattern recognition for payments with minimal remittance data

Technical benchmark: Mature implementations achieve 80%+ auto-match rates with 98%+ accuracy on remittance extraction.

Anomaly detection & risk management AI systems continuously monitor for unusual patterns that might indicate payment risk:

- Payment behavior changes: Sudden shifts in timing, amounts, or communication patterns

- Dispute pattern recognition: Early identification of billing issues before they escalate

- Credit risk assessment: Dynamic scoring based on payment velocity and external data signals

Evaluating "Useful AI" vs. Hype

Explainability requirements Finance teams need to understand and defend AI-driven decisions. Look for:

- Transparent predictions: Clear explanations of why a payment date is predicted or account is prioritized

- Factor visibility: Ability to see which data elements (aging, history, disputes) drive each decision

- Model performance tracking: Regular accuracy measurement and continuous improvement evidence

Human-in-the-loop controls Effective AI augments rather than replaces human judgment:

- Confidence thresholds: Configurable limits for auto-posting with exception routing for edge cases

- Approval workflows: Human review requirements for high-value or unusual transactions

- Override capabilities: Easy ways for specialists to correct AI decisions and improve future performance

Measurable business impact Focus on solutions that can demonstrate concrete improvements:

- Auto-match percentage: Target 80%+ for standard payment types

- Prediction accuracy: Forecast variance within ±10-15% for most customer segments

- Exception rates: Declining manual intervention requirements over time

What to expect from AI in accounts receivable (2025-2026)

Autonomous collections (with guardrails): Advanced systems will handle routine collections activities independently:

- Adaptive messaging: AI-generated follow-up emails within brand voice and policy guidelines

- Dynamic scheduling: Automated call scheduling and calendar integration based on customer preferences

- Escalation triggers: Smart handoffs to human collectors when situations require relationship management

Enhanced forecasting intelligence: Cash flow prediction will become significantly more sophisticated:

- External data integration: Economic indicators, industry trends, customer financial health signals

- Scenario modeling: Multiple forecast scenarios with probability weights and confidence intervals

- Real-time adjustment: Continuous model updates based on new payment data and changing conditions

Integrated risk management: AR AI will connect with broader financial risk systems:

- Credit limit automation: Dynamic adjustments based on payment behavior and external credit signals

- Early warning systems: Proactive alerts for customers showing distress indicators

- Portfolio optimization: Automated strategies for different customer risk and value segments

Practical AI adoption strategy in accounts receivable management

Phase 1: start where data is rich (months 1-3)

- Deploy AI for collections prioritization and basic cash application matching

- Focus on high-volume, standardized transaction types

- Establish baseline metrics for accuracy and efficiency improvement

Phase 2: expand coverage (months 4-6)

- Add predictive payment dating and advanced dispute routing

- Introduce adaptive dunning sequences based on customer response patterns

- Implement automated exception handling for routine adjustments

Phase 3: optimize and scale (months 7-12)

- Deploy autonomous collections for low-risk customer segments

- Integrate external data sources for enhanced prediction accuracy

- Implement cross-functional AI workflows linking AR, sales, and customer success

Implementation success factors

- Data quality: Clean, complete customer and transaction data as foundation

- Change management: Gradual rollout with extensive team training and support

- Continuous monitoring: Regular accuracy measurement and model performance tracking

- Business alignment: Clear ROI measurement tied to DSO, productivity, and forecast accuracy improvements

Metrics to track accounts receivable automation impact

Effective AR automation requires both traditional KPIs to measure outcomes and leading indicators to proactively manage performance. Modern platforms should provide real-time visibility into these metrics with configurable dashboards and automated alerting.

Cash velocity & risk metrics

Days Sales Outstanding (DSO)

- What it measures: Average collection period for credit sales

- How to use it: Track trends alongside aging distribution; avoid over-indexing on DSO alone as it can mask problem segments

- Target ranges: Varies by industry; focus on improvement trajectory rather than absolute benchmarks

- Leading indicators: Aging bucket distribution, promise-to-pay reliability, dispute resolution time

Collection Effectiveness Index (CEI)

- Formula: (Beginning AR + Sales - Ending AR) ÷ (Beginning AR + Sales) × 100

- What it measures: Percentage of collectible receivables actually collected in period

- How to use it: Segment by collector, customer type, and geography to identify performance gaps

- Target range: 95%+ for most B2B environments

- Actionable insights: When CEI drops while activity increases, focus on message effectiveness rather than volume

Average Days Delinquent (ADD)

- What it measures: How far past due customers pay on average

- How to use it: Monitor alongside DSO—rising ADD while DSO stays flat indicates you're backfilling with early payments

- Improvement tactics: Adjust dunning windows, optimize payment methods, escalate high-ADD segments

Promise-to-Pay (PTP) Reliability

- What it measures: Percentage of payment commitments honored on or before promised date

- How to use it: Feed reliability scores back into risk models and forecast weights

- Target range: 75%+ for well-managed programs

- Escalation trigger: Automatic follow-up when PTPs are missed

Operational efficiency metrics

Touches per Paid Invoice

- What it measures: Average number of collection contacts required to secure payment

- How to use it: Identify optimal cadence frequency and channel mix by customer segment

- Improvement indicators: Declining touches with stable or improving CEI

- Segmentation: Track separately for different customer risk tiers and geographies

Time-to-First-Touch (TTFT)

- What it measures: Lag between invoice due date and first collection contact

- Target: Same-day or next-day for high-risk accounts, within 3 days for standard accounts

- Automation opportunity: Rule-based triggers eliminate manual queue management

Auto-Match Rate (Cash Application)

- What it measures: Percentage of payments automatically matched and posted without human intervention

- Target range: 80%+ for mature implementations

- Improvement factors: Better remittance capture, refined matching rules, customer payment behavior training

Exception Rate

- What it measures: Manual interventions required per 100 transactions processed

- How to use it: Track by exception type to identify automation opportunities

- Target trajectory: Declining rate over time as rules improve and edge cases are handled

Dispute & resolution quality

Dispute Rate

- Formula: Disputed invoices ÷ total invoices × 100

- Typical range: 2-8% depending on industry and billing complexity

- Root cause tracking: Tag disputes by reason (pricing, PO mismatch, delivery, billing error)

- Improvement focus: Address top 2-3 dispute causes each quarter through process fixes

Dispute Resolution Cycle Time

- What it measures: Average days from dispute creation to closure

- Target by complexity: Simple disputes <5 days, complex disputes <15 days

- SLA management: Automated routing and escalation based on dispute type and aging

First-Pass Resolution Rate

- What it measures: Percentage of disputes resolved without reopening or additional investigation

- Target range: 85%+ for well-documented processes

- Improvement tactics: Better evidence requirements at dispute intake, cross-functional training

Forecasting & predictive accuracy

Forecast Variance (MAPE/sMAPE)

- What it measures: Error between predicted and actual cash receipts

- Target range: ±10-15% for most customer segments

- Improvement drivers: Better customer behavior data, more frequent model updates, external signal integration

Prediction Confidence Distribution

- What it measures: How often your AI is "confident" vs. "uncertain" in its predictions

- Healthy pattern: Most predictions in high-confidence ranges with accurate low-confidence flagging

- Red flags: Overconfident predictions with poor accuracy, or excessive low-confidence predictions

Customer Health Score Accuracy

- What it measures: How well risk scores predict actual payment delays or disputes

- Validation method: Compare predicted vs. actual payment behavior over 60-90 day periods

- Continuous improvement: Regular model retraining with fresh payment data

Team performance & adoption

Collector Productivity

- Balanced scorecard: Dollars collected per hour, accounts resolved per day, customer satisfaction scores

- Avoid: Pure activity metrics (calls made, emails sent) without outcome measurement

- Coaching focus: Identify high-performing workflows and replicate across team

System Adoption Rate

- What it measures: Percentage of AR activities logged in automation platform vs. external tools

- Target: 95%+ for clean data and accurate reporting

- Improvement tactics: Disable old tools, integrate with daily workflows, provide mobile access

Dashboard Utilization

- What it measures: Weekly active users of AR dashboards and frequency of alert responses

- Best practice: Regular "metrics standups" using real-time data to drive daily decisions

- Success indicator: Management questions shifting from "what happened?" to "what should we do next?"

Advanced analytics & benchmarking

Portfolio Segmentation Performance

- Analysis: Compare DSO, CEI, and dispute rates across customer segments (geography, size, industry)

- Action triggers: Segments performing 20%+ worse than average need dedicated strategies

- Opportunity sizing: Calculate cash impact of bringing underperforming segments to benchmark levels

Channel Effectiveness

- Measurement: Response rates, payment conversion, and customer satisfaction by communication channel

- Optimization: A/B testing of email templates, phone scripts, portal messaging

- Personalization: Customer preference learning and adaptive channel selection

Competitive Benchmarking

- Industry DSO comparisons: Understand relative position and improvement opportunity

- Best practice identification: Regular benchmarking studies and peer group participation

- ROI validation: Quantify automation impact against industry baselines

Implementation note: Start with 5-7 core metrics (DSO, CEI, auto-match rate, dispute cycle time, forecast accuracy) and expand measurement sophistication as processes mature. The goal is actionable insights, not measurement overwhelm.

Future of AR automation(2025-2027)

The next three years will see accounts receivable evolve from automated processes to intelligent, self-optimizing systems. This transformation is driven by advances in artificial intelligence, real-time payment infrastructure, and integrated financial platforms.

Real-time payment infrastructure impact

Instant settlement, delayed data: While real-time payment rails (FedNow, RTP) continue rapid adoption, the "data about the money" often arrives separately from the payment itself. Federal Reserve research emphasizes the need for standardized remittance to unlock automation benefits, with ISO 20022 providing the technical framework for richer payment data.

What this means for AR teams:

- Immediate impact: Same-day cash availability with potential next-day reconciliation gaps

- System requirements: Enhanced remittance capture and parsing capabilities for multiple data streams

- Process changes: Real-time payment notifications feeding dynamic dunning pause/resume logic

Preparation strategy: Integrate bank APIs for instant payment notification while building robust remittance data capture from email, portal, and structured message formats.

From rules-based to autonomous AR

Governed Autonomy Model: Deloitte's finance transformation research and Accenture's CFO studies point toward "autonomous finance"—systems that handle routine decisions independently while escalating exceptions to humans. In AR, this manifests as:

- Adaptive collections: AI-generated follow-up messages within brand guidelines and policy constraints

- Dynamic prioritization: Continuous work queue optimization based on response patterns and payment probabilities

- Intelligent escalation: Automated handoffs to human collectors when relationship management or complex negotiation is required

Control Framework Requirements:

- Confidence thresholds: Automated decision-making only within defined accuracy ranges

- Audit trails: Complete logging of AI decisions and human overrides

- Performance monitoring: Real-time accuracy tracking with automatic model retraining

Integrated Receivables as Operating Model

Breaking down data silos: Leading companies are unifying AR, AP, and treasury data to manage liquidity continuously rather than reactively. This "integrated receivables" approach connects:

- Customer payment behavior with supplier payment terms for net working capital optimization

- Real-time cash position with AR forecasts for dynamic investment decisions

- Credit risk signals with sales pipeline data for proactive account management

Technology enablers:

- Open banking APIs: Direct connectivity between AR systems and bank accounts

- Cloud data platforms: Real-time synchronization across ERP, CRM, and treasury systems

- AI-powered reconciliation: Automated matching across multiple data sources and formats

Enhanced customer experience standards

Consumer-grade B2B expectations: McKinsey research highlights the paradox of "simpler interfaces, complex reality"—buyers expect consumer-level simplicity while backend operations become more sophisticated. For AR, this means:

Self-service excellence:

- Intelligent payment portals: Predictive payment suggestions based on customer cash flow patterns

- Proactive communication: Automated alerts before issues arise rather than reactive collections

- Contextual assistance: AI-powered help that understands customer history and preferences

Relationship-aware automation:

- Tone adaptation: Communication style adjustment based on customer relationship value and payment history

- Channel optimization: Automatic selection of preferred communication methods by customer

- Escalation sensitivity: Human handoff triggers based on account value and relationship complexity

Cross-border & regulatory evolution

ISO 20022 and richer data standards The global shift toward ISO 20022 messaging standards enables significantly richer payment data, but requires AR systems capable of processing hundreds of potential data elements. Early adopters will gain competitive advantage through:

- Straight-through processing: Higher auto-match rates from structured remittance data

- Enhanced analytics: Deeper insights from granular payment information

- Reduced exceptions: Fewer manual interventions due to complete payment context

Regulatory compliance integration E-invoicing mandates and real-time tax reporting requirements across global markets will drive AR process standardization:

- Automated compliance: Built-in regulatory requirement checking and reporting

- Multi-jurisdiction support: Seamless handling of different regional requirements

- Audit automation: Real-time compliance monitoring and exception reporting

Practical preparation framework

90-day quick wins

- Connect money + data: Pilot integrated receivables with primary banking partner

- Implement real-time sync: Upgrade ERP connectivity for instant payment notification

- Deploy governed autonomy: Define confidence bands for automated posting and escalation rules

- Establish liquidity process: Weekly AR/AP/treasury data integration for cash management

12-month strategic initiatives

- AI model maturity: Develop explainable prediction models with confidence scoring

- Customer experience enhancement: Deploy self-service portal with intelligent assistance

- Cross-functional integration: Link AR data with sales pipeline and customer success metrics

- International standardization: Prepare for ISO 20022 adoption and multi-currency complexity

24-month transformation

- Autonomous operations: Achieve 80%+ automated transaction processing with human oversight

- Predictive cash management: Real-time liquidity optimization across all financial processes

- Customer relationship intelligence: AI-powered account management recommendations

- Continuous optimization: Self-improving processes with minimal manual intervention

Success measurement evolution with AI-powered AR

Traditional KPIs (still important):

- DSO improvement

- Collection effectiveness

- Cost reduction

Emerging KPIs (increasingly critical):

- Forecast accuracy: How well do predictions match actual cash flow?

- Customer experience scores: Are automated processes enhancing or degrading relationships?

- Process intelligence: How effectively do systems learn and improve?

- Integration efficiency: How seamlessly do AR processes connect with broader financial operations?

Future-ready organizations will measure AR success not just by cash collection speed, but by contribution to overall financial agility, customer satisfaction, and strategic decision-making capability.

The companies that begin this evolution now—building explainable AI, implementing real-time data integration, and designing customer-centric automation—will have significant competitive advantages as these trends accelerate through 2027.

FAQ & Glossary

Frequently asked questions

Q: How long does AR automation implementation typically take? A: Implementation timelines vary by scope and complexity:

- Basic collections automation: 4-6 weeks

- Collections + cash application: 8-12 weeks

- Full-scale transformation (all modules): 12-20 weeks

Success factors include data quality, integration complexity, and change management approach. Companies with clean master data and dedicated project teams move fastest.

Q: What's the realistic ROI timeline for AR automation? A: Most organizations see positive ROI within 6 months, with payback often occurring in the first quarter. Typical benefits progression:

- Month 1-2: Process efficiency gains, reduced manual effort

- Month 3-4: Measurable DSO improvement, faster dispute resolution

- Month 6+: Compounding benefits from improved forecasting and customer relationships

Q: Can AR automation work with our existing ERP system? A: Modern AR platforms integrate with all major ERPs including NetSuite, SAP, Microsoft Dynamics, QuickBooks, and Sage. Key considerations:

- Real-time vs. batch sync: Look for platforms offering real-time bi-directional integration

- Custom field support: Ensure your ERP's unique fields and workflows are supported

- API quality: Robust APIs enable better integration than file-based connections

Q: How do we handle customers who prefer phone calls over automated emails? A: Effective AR automation accommodates customer preferences rather than forcing channel adoption:

- Preference management: Portal settings allowing customers to select communication channels

- Hybrid workflows: Automated scheduling for phone-preferred customers with manual call execution

- Intelligent escalation: Rules-based handoff from automated to personal outreach based on customer value and response patterns

Q: What happens to our AR team when processes are automated? A: Automation shifts team focus from routine tasks to strategic work:

- Role evolution: Collections specialists become relationship managers and exception handlers

- Skill development: Training on analytics, customer relationship management, and strategic collections

- Capacity reallocation: Time freed from data entry and manual follow-up enables focus on complex disputes and high-value accounts

Q: How accurate is AI-powered payment prediction? A: Mature AI models achieve 80-90% accuracy for most customer segments when predicting payment dates within ±7 days. Accuracy depends on:

- Data quality: Clean payment history and customer interaction data

- Model sophistication: Multi-factor analysis vs. simple trending

- Continuous learning: Regular model updates with fresh data

Q: Can we start with just collections automation and add cash application later? A: Yes, phased implementation is often the most successful approach:

- Phase 1: Collections and dunning automation to prove value quickly

- Phase 2: Add customer portal and dispute management

- Phase 3: Implement cash application and advanced forecasting

This approach allows teams to build confidence and demonstrate ROI before tackling more complex processes.

Q: How do we ensure compliance with international regulations? A: Leading AR platforms include built-in compliance features:

- Data privacy: GDPR, CCPA compliance with appropriate data handling and retention

- Financial regulations: Support for regional accounting standards and reporting requirements

- Communications compliance: Adherence to debt collection regulations by jurisdiction

- Audit trails: Complete activity logging for regulatory examination

Q: What's the difference between AR automation and AR software? A: AR software typically refers to basic invoice management and reporting tools. AR automation encompasses intelligent workflows that handle routine tasks without human intervention:

- Software: Manual processes with digital tools

- Automation: System-driven processes with exception handling

- Intelligence: Predictive capabilities and self-optimization

Glossary of key terms

Accounts Receivable (AR): Money owed to a company by customers for goods or services delivered on credit.

Aging Report: Analysis of outstanding invoices categorized by how long they've been overdue (current, 30-60 days, 60-90 days, 90+ days).

AI-Powered Matching: Machine learning algorithms that match incoming payments to outstanding invoices using pattern recognition and historical data.

Auto-Posting: Automated entry of payment transactions into the ERP system without manual intervention.

Average Days Delinquent (ADD): Average number of days past due date that customers actually pay.

Cash Application: Process of matching incoming payments to outstanding invoices and posting to the appropriate accounts.

Collection Effectiveness Index (CEI): Metric measuring the percentage of collectible receivables actually collected in a given period.

Days Sales Outstanding (DSO): Average number of days it takes to collect payment after a sale.

Dunning: Systematic process of communicating with customers to collect overdue payments.

Exception Handling: Process for managing transactions that don't fit standard automated workflows.

Explainable AI: Artificial intelligence systems that provide clear reasoning for their decisions and predictions.

Forecast Variance: Difference between predicted and actual cash receipts, typically measured as Mean Absolute Percentage Error (MAPE).

ISO 20022: International standard for financial messaging that enables richer, more structured payment data.

Lockbox: Banking service where customer payments are sent directly to a bank for processing rather than to the company.

OCR (Optical Character Recognition): Technology that extracts text data from images and PDFs, commonly used for remittance processing.

Payment Application: Process of allocating received payments against specific invoices or accounts.

Promise-to-Pay (PTP): Customer commitment to pay by a specific date, tracked and followed up automatically.

Real-Time Payments (RTP): Instant payment systems that enable immediate settlement 24/7/365.

Remittance Advice: Document accompanying a payment that details which invoices are being paid.

Straight-Through Processing (STP): End-to-end transaction processing without manual intervention.

Unapplied Cash: Payments received but not yet matched to specific invoices or accounts.

Working Capital: Short-term assets minus short-term liabilities; AR represents a significant component of working capital.

That's AR automation. Whether it's worth the effort depends on how much you're losing to manual processes right now. Schedule a demo to see how Growfin's AI-powered AR automation can accelerate your cash flow and reduce manual effort.

.webp)

.webp)

.webp)

.webp)