.png)

.webp)

.webp)

.webp)

Every AR analyst has seen this happen.

A payment comes in. The amount is close, but off. Sometimes it's a 2% discount. Sometimes a bank fee. Sometimes a deduction for damaged goods, a contract milestone holdback, or a cryptic remittance note with no explanation attached.

Short payments are the single largest driver of exception volume in cash application. The $200 variance that takes 5 minutes to identify can take 45 minutes to investigate, classify, and resolve.

This guide breaks down why short payments create so much friction, where static reconciliation rules fall apart, and how adaptive adjustment handling is changing the way finance teams close invoices.

The real cost of short payments in AR

A short payment is a payment received for less than the invoiced amount, typically caused by early payment discounts, contractual holdbacks, bank fees, or operational deductions.

Most AR processes are built on a simple assumption: invoice amount equals payment amount. In practice, payments rarely arrive that cleanly. Customers take early payment discounts. Contracts include negotiated deductions. Banks apply transfer fees. Operational disputes lead to short pays. International payments introduce currency rounding variances.

Every large customer eventually develops its own payment behavior. The challenge is that these differences rarely arrive in structured formats.

AR teams are forced to piece together context from:

- Bank statements

- Remittance emails and PDFs

- Customer portals

- ERP records

- Historical payment patterns

- Tribal knowledge inside the finance team

That search for context is what slows reconciliation down. In many organizations, resolution logic lives across shared inboxes, spreadsheets, ERP notes, and the memory of experienced analysts who simply know how certain customers pay.

When an analyst receives a payment that's short by $200, the investigation begins:

- Is this an approved deduction?

- Is it a pricing discrepancy?

- Did the customer apply a valid discount?

- Is this a bank fee?

- Is the deduction recurring?

- Has this customer done this before?

- Should the invoice be closed, disputed, or escalated?

- Does someone need to approve the adjustment?

Multiply this across hundreds of payments per week, and the downstream effects are predictable: delayed cash posting, growing unapplied cash, slower month-end close, increased DSO, and manual operational overload.

The gap between high-performing AR teams and everyone else often comes down to how efficiently they handle exceptions. Short payments are one of the biggest reasons teams stay stuck with slow cash posting and delayed close cycles.

Where static reconciliation logic breaks down

Static tolerance rules were designed for a world where payment behavior was relatively predictable. Most AR systems handle adjustments with fixed logic:

- If the variance is under $50, auto-write off.

- If the customer takes a 2% discount within 10 days, accept the deduction.

- If the reason code matches a known category, route to disputes.

These rules work in controlled environments. B2B payment environments are anything but controlled.

One customer sends structured remittance files. Another sends handwritten references in PDFs. One region deducts bank charges consistently. Another bundles multiple deductions into a single payment. A customer who historically paid cleanly changes behavior after renegotiating terms.

Fragmented and missing remittance data remains one of the most persistent challenges for cash application teams. Adding more rules only patches the surface, because customer payment behavior keeps changing, and static logic can't learn from prior resolution patterns.

The result: analysts end up re-investigating the same categories of deductions every month. Operationally valid deductions continue to behave like unresolved exceptions. Analyst time goes toward routine payment differences rather than cases that genuinely require judgment.

What adaptive adjustment handling looks like in practice

Adaptive adjustment handling separates payment differences into two categories:

- Routine, explainable adjustments

- True exceptions requiring investigation

That distinction matters. Most short payments are operationally valid. If a customer consistently takes approved discounts, deducts known fees, or follows contractual payment structures, forcing analysts to manually review every one of those transactions adds no value.

A stronger workflow should be able to:

- Recognize recurring customer payment behaviors

- Classify variances against historical patterns

- Apply standardized resolution logic consistently

- Escalate only when confidence is low or context is missing

The shift changes where AR teams spend their time. Fewer routine deductions, more focus on ambiguous, high-risk, or genuinely unresolved transactions.

For example, if a customer repeatedly deducts freight charges under similar invoice conditions, the workflow can recognize that pattern and handle it consistently, rather than forcing an analyst to revisit the same investigation every month.

That consistency matters more than most teams realize. In many organizations, analysts resolve the same categories of deductions month after month simply because prior decisions aren't retained or reused operationally.

The strongest adjustment workflows share a common trait: they reduce repetitive review work while keeping exceptions visible, traceable, and auditable. The goal is to reserve analyst time for cases that require judgment.

Short payment scenarios finance teams see every week

A large portion of short payments aren't disputes. They're expected deductions that sit in review queues because the workflow sees a mismatch, not the context behind it.

Early payment discounts.

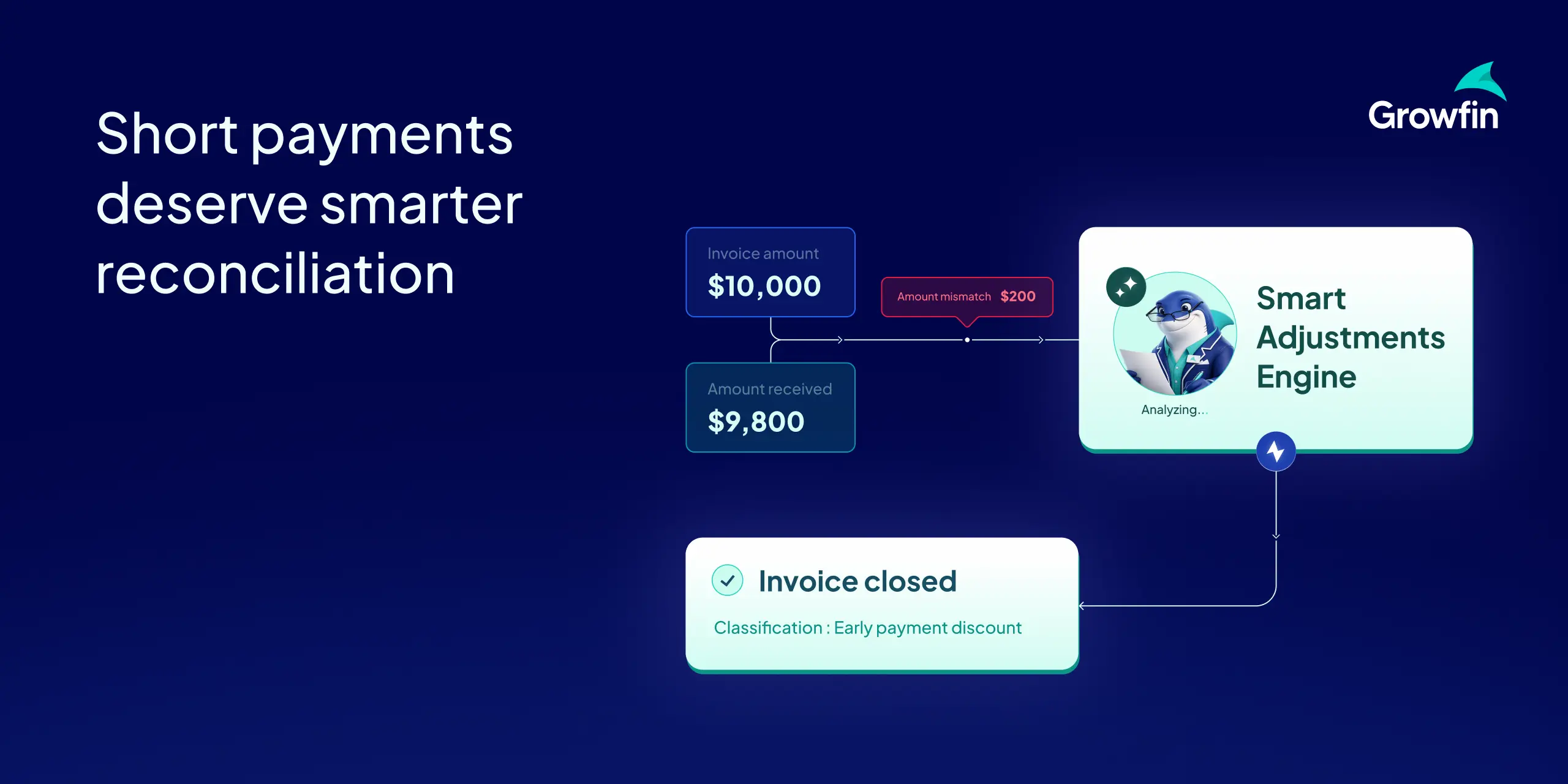

A customer on 2/10 NET 30 terms pays a $10,000 invoice early and sends $9,800. The 2% discount is contractually valid. But if the workflow treats every short payment the same way, the analyst still stops, verifies, and manually clears the invoice.

Milestone-based holdbacks.

A customer holds back 10% until implementation is complete, paying $4,500 on a $5,000 invoice. Teams usually know this arrangement exists, but unless the workflow accounts for contractual context, the deduction lands in an exception queue.

Operational deductions.

A retailer deducts an approved damage claim from a shipment payment, reducing a $2,000 payment to $1,700. That deduction often moves through AR, operations, and disputes, even when the claim was already approved.

Wire fees, tax rounding, and partial references.

None of these are unusual on their own. The problem is volume. Over time, finance teams spend a disproportionate amount of effort reviewing payment differences that are repetitive, explainable, and operationally familiar.

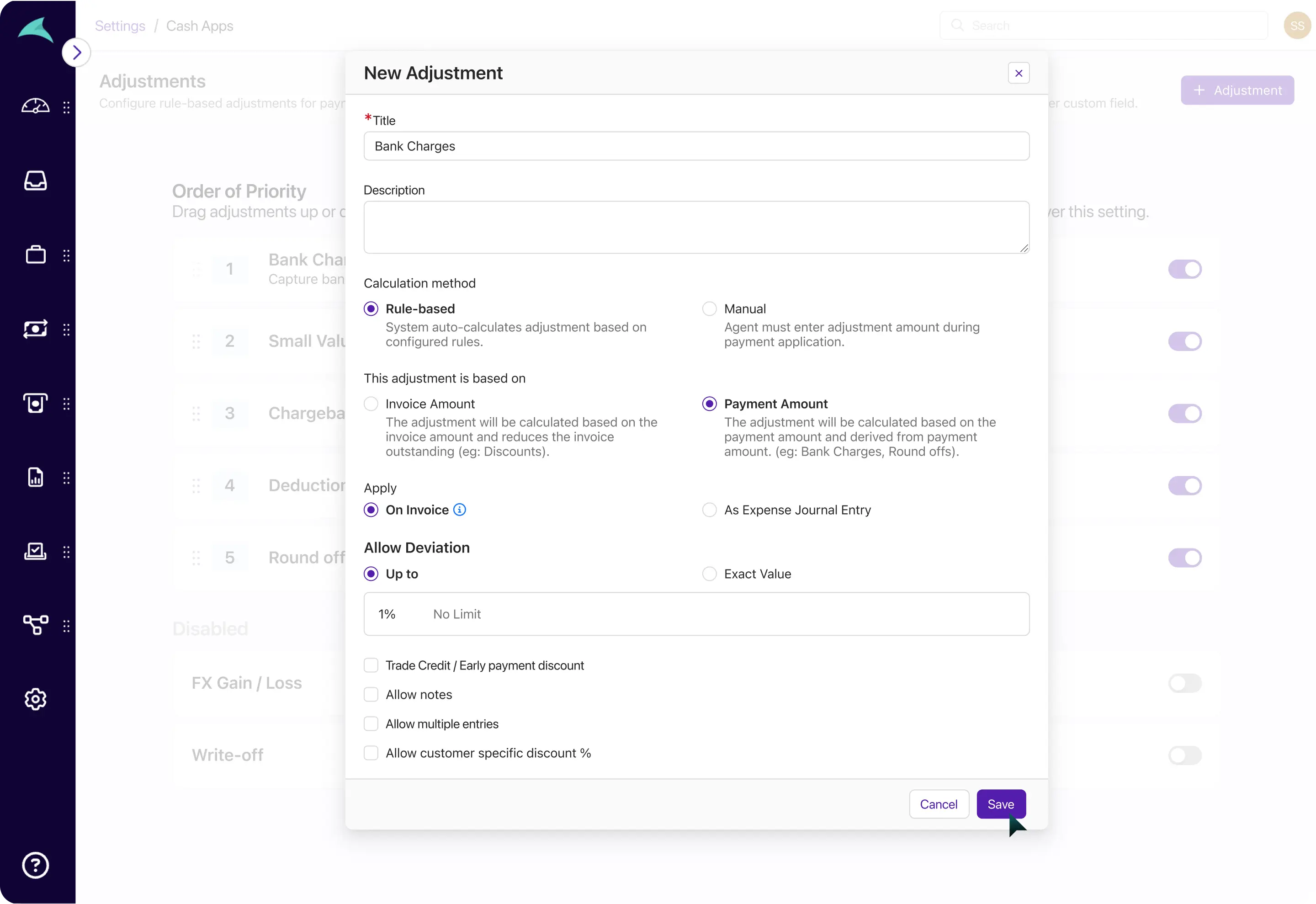

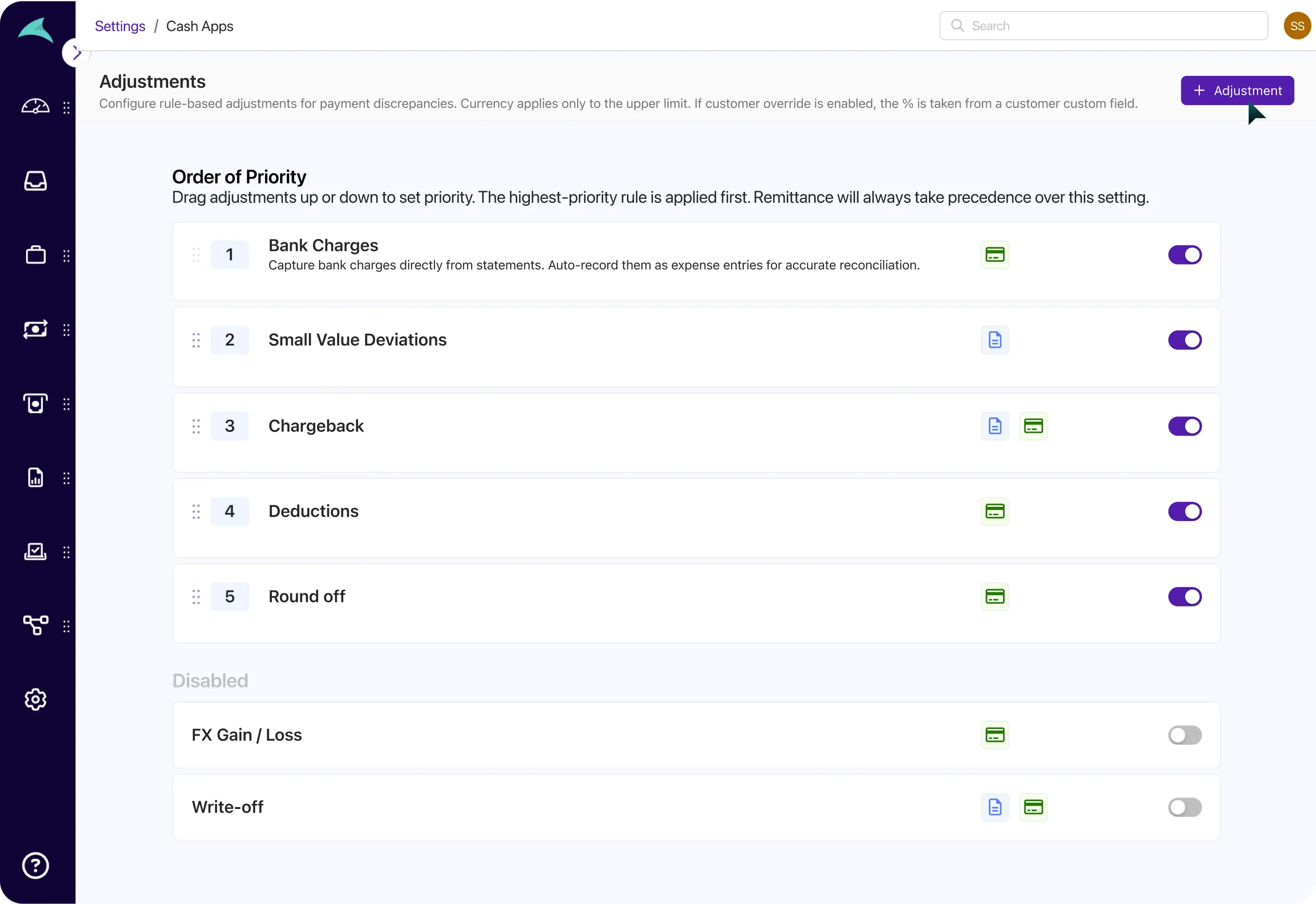

How Growfin's Smart Adjustments Engine handles short payments

Growfin recently launched the Smart Adjustments Engine inside its cash application product to address exactly this problem.

When a payment is received, the engine:

- Compares the payment amount against the invoice

- Detects any variance automatically

- Evaluates the difference against configured adjustment rules and historical patterns

- Routes the outcome: valid deductions are applied and the invoice is closed; unclear or material exceptions are flagged for the right team to review.

The difference from static rules: the Smart Adjustments Engine handles both invoice-level and payment-level adjustments, supports multiple adjustments on a single payment, uses priority-based logic to resolve conflicts, and adapts dynamically to remittance data, bank file patterns, and prior analyst decisions.

It was built for the messy reality of B2B payments, where remittance formats vary by customer, deduction habits change over time, and payment context arrives fragmented across email, PDFs, and bank files.

For AR teams running high transaction volumes, the practical impact is significant:

- Faster same-day cash posting by eliminating manual reviews on routine deductions

- Consistent handling of deductions across regions and teams

- Clearer visibility into deduction patterns that signal revenue leakage or operational issues

- Standardized adjustment logic that doesn't depend on individual analyst experience

Short payments are an AR workflow problem, not a matching problem

The real bottleneck in reconciliation is rarely invoice matching itself. It's the growing volume of payment exceptions that sit between "fully matched" and "fully unresolved." That gray area is where finance teams spend most of their time.

Reconciliation is becoming less about matching amounts and more about understanding why customers pay the way they do.

That understanding is where adaptive adjustment handling, and tools like Growfin's Smart Adjustments Engine, create the biggest impact.

See how our Adjustments Engine works.

TL;DR

- Short payments are the top driver of manual work in cash application, consuming the majority of AR team time.

- Static reconciliation rules can't adapt to changing customer behavior, fragmented remittance data, or evolving deduction patterns.

- Adaptive adjustment handling separates routine deductions from true exceptions, reducing repetitive investigation work.

- Growfin's Smart Adjustments Engine automates short payment resolution by learning from remittance patterns, configured rules, and prior analyst decisions.

- The goal: reserve analyst time for cases that require judgment, not routine pattern matching.

.webp)

.webp)

.webp)

.webp)