.png)

.webp)

.webp)

.webp)

Cash applications don't make it on a board deck; instead it sits inside AR spreadsheets, quietly turning data from bank statements, and remittance fragments into cleared invoices.

But when it fails (which almost always happens); it doesn’t fail locally. It fails at the level that board members care about:

- unreliable cash visibility

- month-end close volatility

- audit irregularities

- finance teams spending time reconciling the past; instead of strategizing for the company

In spite of this, the current scenario remains the same; most leaders still treat cash application as a “back-office” hygiene task that can either be solved by throwing more people at the problem or hopefully matching and hoping that it is accurate. Some teams have done it differently and have fully automated it; by without any human checkpoints. In reality, both paths have created chaos.

Let’s dwell a little deeper into the messy reality: payment methods proliferate, remittance data is semi-structured at best, and almost always delayed, customer behaviour changes faster than a startup’s product roadmap. Manual cash application collapses under that complexity.

So what’s the opportunity? To design a cash application operating engine that is AI-powered to understand patterns at scale, while having humans intentionally positioned at the right exception checkpoints. That’s how you eliminate chaos and still close books on time.

How cash application became the blind spot in AR modernization

From a leadership vantage point, your AR stack has definitely evolved: there’s ERP at the core, enabling invoicing and collections, and there are also workflows that exist to simplify processes (a little!). However, at the same time, cash application remains a patchwork of:

- Payment method proliferation – ACH, wires, cards, digital wallets, international transfers, even crypto in some industries, all landing in different bank formats.

- Fragmented remittance – emails, PDFs, customer portals, lockbox files, spreadsheets, and check images, all with inconsistent structures and IDs.

- Customer-specific “puzzles” – every large customer has its own conventions: internal reference numbers instead of your invoice IDs, recurring adjustments, idiosyncratic payment schedules.

- Adjustments and deductions – taxes, bank fees, discounts, partial payments, disputes. Each one demands judgment on how to allocate and code it.

- Month-end pressure – as close approaches, the backlog of unapplied cash delays reporting and planning.

In an mid-sized logistics enterprise, an AR specialist reported spending 6–7 hours every day just matching payments to invoices, building mental models of cryptic customer behavior that lived only in her head. If she walked out, the pattern recognition walked out with her.

At a distance, this looks like an efficiency problem. Up close, it’s a structural risk:

- Key cash-flow knowledge is trapped in individuals.

- The posting lag between “cash in bank” and “cash in system” becomes unpredictable.

- FP&A and treasury cannot rely on near-real-time collections data.

- The audit trail for how payments were allocated is fragile and scattered.

That is the hidden cost: cash application is where your organization silently decides how real your reported cash position actually is.

The true cost of manual cash application

When finance teams model the cost of manual cash application, typically they see FTEs plus some overtime. But that’s just the tip of the iceberg. The real drag shows up across four dimensions: FTE, Liquidity, Close & Audit, Opportunity Cost.

Let’s start with the obvious - the number of people and FTE hours.

FTE Drag: A typical cash application team in a mid market or enterprise might have 1-3 cash application specialists. Let’s assume half their time is spent on manual matching, remittance decoding, spreadsheet reconciliation, working on deductions, and posting to the ERP. This ultimately means your highly talented collection team are acting as parsers and doing what an intelligent system can do much more reliably.

You don’t need an external benchmark to quantify this. You can calculate it directly:

Annual FTE Drag = FTEs × % of time on cash app × FTE Cost

For example, if you have 3 FTEs spending 60% of their time on cash applications at a cost of $60k, you’re spending ~$108k a year just on pattern matching and data entry. And that is before any of the indirect costs comes into the picture.

In one AI-enabled implementation, an enterprise of ours moved from multiple specialists working primarily on cash application to a single person spending just 30-40% of their time reviewing exceptions, with the system handling 80%+ payments autonomously.

The human work in cash application should just be about exception and governance, not brute-force matching.

Liquidity Drag: Manual cash application also creates a liquidity drag; basically cash that has hit your bank but not your decision-making. When posting lags by several days, treasury sees a distorted picture which has major implications:

- Short-term debt payments get delayed

- Investments and discretionary spending slows down because there’s no distinction between truly free cash and unapplied cash

- The trust on cash inflows isn’t there; hence there’s a need to always have higher operational cash buffers for enterprise functioning

You don’t need an external benchmark to quantify this either. You can calculate it directly:

Annual liquidity cost = [average daily receipts × average posting delay in days] × cost of capital

Therefore, if you collect $2million a day, and your average posting delay is 3 days, that’s $6million in cash that is not reliably visible in your systems; and thus in your decision making as well. At a 5% cost of capital, that’s roughly ~$300K a year in liquidity costs; without counting the strategic decisions that you delay because you’re flying with blurred instruments.

Close & Audit Drag: Manual cash applications doesn’t just slow down the close; it makes it inconsistent:

- During some months, the team works overtime, becomes heroic, and clears unapplied cash; during other months, backlog spills into Week 2 or 3.

- Reconciling partial payments, and complex deductions becomes a month-end detective game, with different collectors making heavily biased judgement calls.

From a leadership perspective, this matters because:

- Audit risk increases when decision-making is done based on information present in emails, spreadsheets, or individual memory instead of a smart engine that uses AI for decision making, and leaves an audit trail.

- If payments are misapplied and surface weeks or months later, it creates fractures between internal teams, impacting future collections. Complications multiply.

Opportunity Cost: Every hour your senior AR analysts spend decoding remittance PDFs, this is what they aren’t doing:

- undisturbed focus on exceptions, and presence at human checkpoints where subjective judgement matters.

- working strategically with other teams like treasury and FP&a on cash forecasting and its accuracy

- optimizing customer payment behaviour to improve cash flows

Why 100% automation backfires in cash application

Confronted with these costs, the instinctive leadership response is then “Okay, let’s automate every step of the way”. But in cash application, full automation without guardrails gives you a different failure mode:

- The system confidently posts payments using rules that don’t keep up with the increasing types of customer behaviour.

- Edge cases like new customers, unusual deductions, multiple entities are treated like normal matching cases.

- There is no explainability or audit trail when something breaks on why the match was made.

Whereas, the most effective operating models use several layers of intelligence:

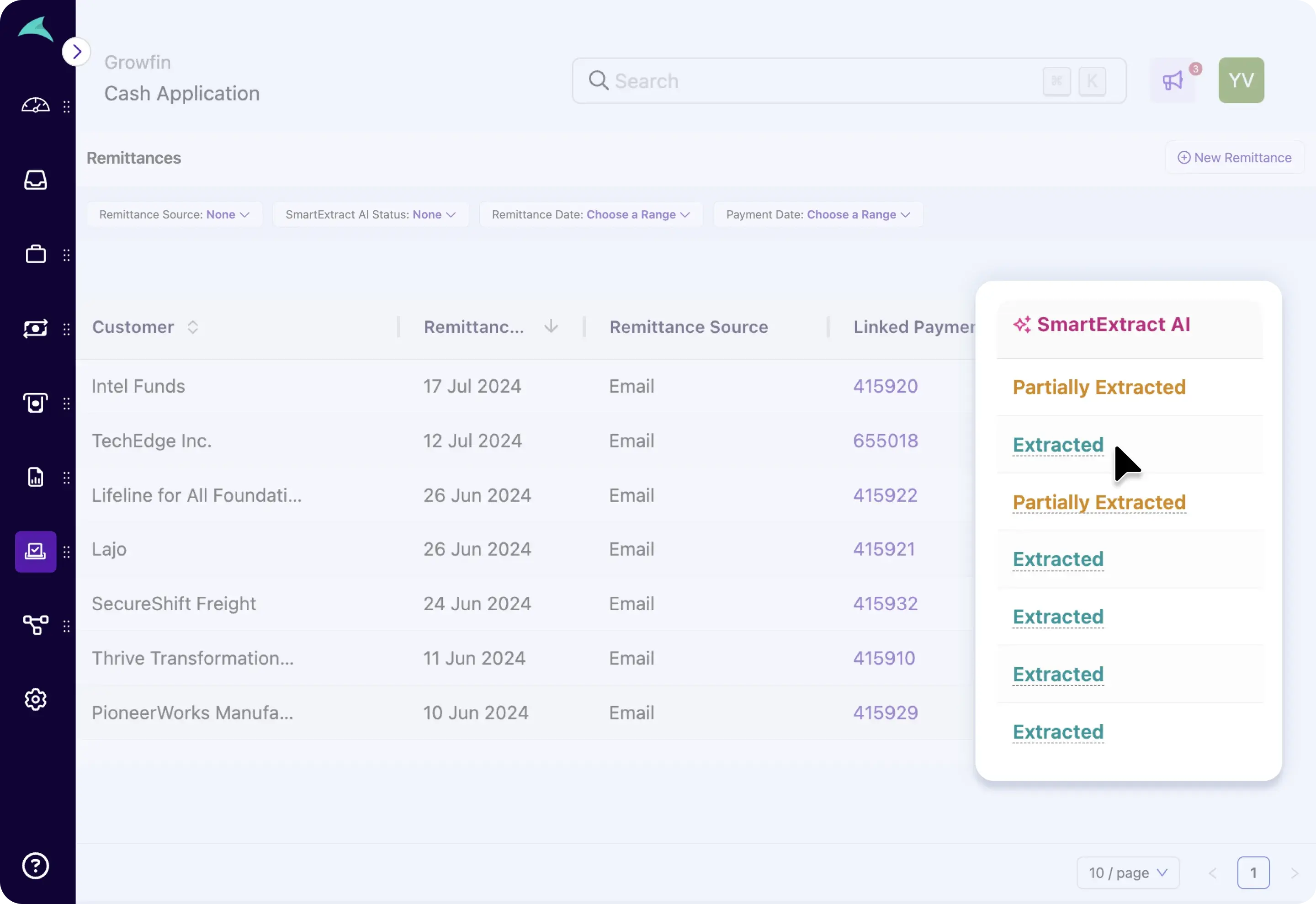

- Multi-source remittance capture from banks, emails, lockboxes, and files with automation to extract data across PDFs, CSVs, check images, and other semi-structured sources.

- Pattern recognition and fuzzy matching that learns how each customer pays, accommodating their reference numbers, formats, and historical behavior rather than relying on rigid rules.

- Confidence scoring on every proposed match, automatically processing high-confidence scenarios and flagging ambiguous or unusual ones for review.

- Exception workflows and audit trails, so humans can focus on resolving complex cases with full context, not digging for it.

Under this model, “perfect AR” doesn’t mean “no humans.” It means:

- The machine does 80–95% of the work where patterns are clear.

- Humans own the design of policies, the review of low-confidence cases, and the governance of the system.

What do you gain? Both speed and control. And you avoid the nightmare of confident, opaque mis-postings that only surface at audit time.

A framework to remove chaotic cash application

To move away from manual chaos, cash application needs a reference design which enables finance leaders to have a holistic view of their unapplied cash and its impact from a 30,000 feet perspective.

Here’s a practical framework with five design decisions:

1. Define Your Signal Universe

Map every source of payment and remittance signal:

- Bank feeds and formats (BAI, MT940, etc.)

- Lockbox services and check images

- Customer portals and EDI feeds

- Emails and attachments (PDFs, CSVs, spreadsheets)

Your goal: a single ingestion layer that can see and standardize all of these, instead of parallel, semi-manual workflows owned by different teams.

2. Elevate the Matching Engine from “Rules” to “Behavior”

Legacy matching logic treats payments as static patterns. Modern engines:

- Learn customer-specific behaviors (e.g., always referencing POs, always netting discounts).

- Apply fuzzy logic to tolerate typos, partial information, and formatting discrepancies.

- Use historical context (prior payment history, recurring adjustments) to inform decisions.

3. Put Human Judgment at Explicit Checkpoints

Instead of humans hunting for problems, design structured checkpoints around:

- Low-confidence matches (below a defined threshold).

- High-value payments above a certain amount.

- Complex allocation types: multi-entity payments, unusual deductions, or out-of-policy discounts.

This is where your most experienced AR professionals should sit; not in the middle of a remittance parsing queue, but at decision gates where their judgment actually changes risk.

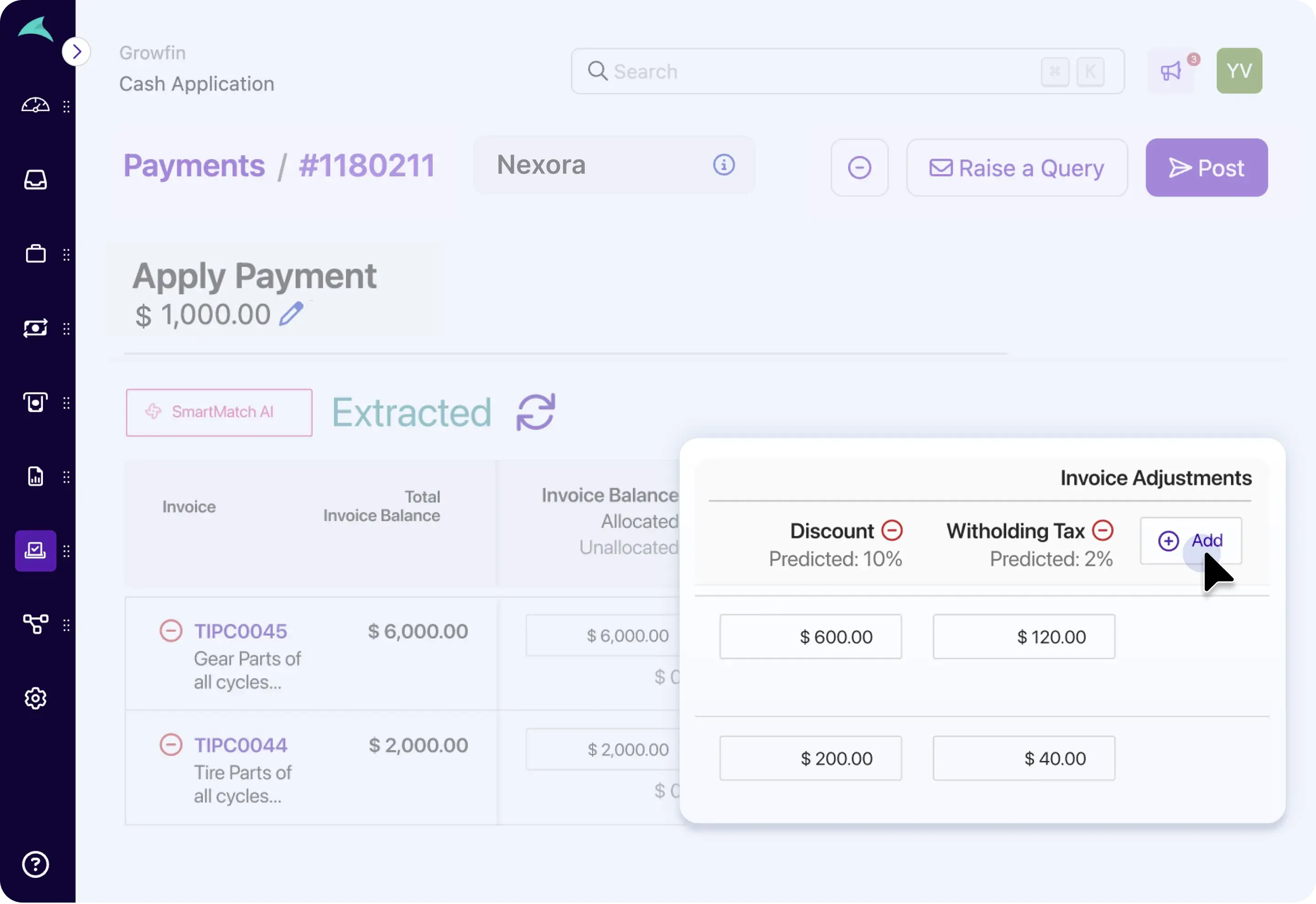

4. Encode Adjustments and Policy into the System

The nastiest cash application work usually lives in partial payments, deductions, and adjustments. A modern setup should:

- Automatically identify common deductions (taxes, bank fees, FX, discounts).

- Apply policy-aligned allocation rules for partial payments (e.g., oldest invoice first, or by risk bucket).

5. Close the Loop: Metrics, Feedback, and Governance

Finally, a no-chaos model needs a feedback loop:

- Every automated decision carries a confidence score and rationale, captured in an audit trail.

- Manual overrides feed back as training signals, improving future accuracy.

- You track a small set of leadership-level KPIs:

- % of payments posted same day

- % of cash auto-applied vs requiring human touch

- Average unapplied cash balance

- Manual hours per $1M of cash collected

- Days to first close and variability over time

This is where finance leaders can have the most impact: governing the system like a product, not a one-time project.

What does this mean for finance leadership?

If you continue to let manual cash application to run circles around your AR teams, and consider it as “just an operational detail”, you’ll keep paying for it in liquidity, close volatility, and credibility with your board, and auditors.

On the other hand, if you buy into the myth that Perfect AR = 100% Automated AR, you’ll chase after a fully automated black box while its blind spots only double your headache.

There’s a third option; a highly distinguishable leadership move:

- Treat cash application as a strategic proving ground for AI powered AR; where you can show that human-in-the-loop automation delivers faster, cleaner books, and stronger control.

- Redefine “Perfect AR” inside your organization as “highly automated + intentionally human”

And, the next time you get questioned “How confident are we in the cashflows that we presented to the board” - it won’t be a guess; neither would it be simply close; it’d be near perfect numbers generated by a cash application engine you actually understand and govern.

.webp)

.webp)

.webp)

.webp)